This guide was published on April 9, 2020.

Leading a startup has always been challenging, even under the best conditions. Founders need to quickly master a tremendous range of skills, from building a fantastic product and nailing go-to-market efforts to raising money and managing a board, all while figuring out hiring, culture and compensation. Starting a company is also a lonely endeavor, one that forces founders to make difficult decisions every day with imperfect information. While triaging these challenges, eventually every founder runs headfirst into a problem they haven’t seen before, the kind that leaves them unsure of where to start.

In April 2020, we’re decidedly not operating in the best of conditions. With a future that’s more cloudy than clear, the dynamics founders face are magnified many times over and playing out simultaneously — at warp speed. Whatever tactics and strategies were working in January, chances are they’re not as effective now.

These increasingly unmooring circumstances are the ultimate test of a leader’s resilience. In our experience, the best safety net is the wisdom of the community and the experience of fellow entrepreneurs. There’s no shortage of content out there right now on how COVID-19 is affecting startups. But amid the explosion of writing on the pandemic and the advice we’ve all seen scattered across Twitter threads, Substack newsletters and Medium posts, we’ve found that there are still very few resources that dig deeply into the nitty-gritty “how” of leading and planning during this crisis.

Over the past several weeks, we’ve been fielding a wide array of questions from First Round-backed founders:

- How do we approach planning given COVID-19?

- What signals should we be watching before pulling the trigger on alternative spending plans?

- How will the bar for fundraising be different in 18-24 months compared to now?

- Are there any alternatives to a RIF while still decreasing burn?

- How do we market during these times?

As for the answers, we have our own takes, of course. Since our start in 2004, the First Round team has applied a long-range lens through every twist and turn in the market. Partners Josh Kopelman and Bill Trenchard were building companies in the early 2000s, and were on the investing and advising side in 2008, helping companies like Square and Uber navigate choppy waters as the economy recovered from the Great Recession. We firmly believe, however, that the best company-building advice doesn’t always come from venture capitalists. More often, it comes from the peers and practitioners — the ones who’ve either been in your shoes before or are shoulder-to-shoulder with you in the trenches right now.

That’s why we’ve attempted to crowdsource and curate the lessons we’ve come across for this guide. Some of the advice we share here will come from the First Round team, some of it from founders who’ve built in downturns before, and some from resources we've curated. We’ve done original interviews, culled from previously-unpublished First Round Community guides and surveyed founders on how they’re planning to weather the storm. As ever, we’ll be highlighting what we find important, overlooked or counterintuitive.

We appear to be in the early innings, so there are no perfect answers or fully-baked playbooks here. But by sharing initial thinking, talking about the challenges everyone is facing and harnessing the helpful advice floating around in private channels, we hope to help you shape — and relentlessly refine — your response as the situation on the ground continues to change quickly.

We’re thankful to every startup leader who took the time to generously share their hard-won wisdom — particularly those who have previous experience building in the dot-com era and the Great Recession. Although we’re living in unprecedented times and every path is unique, we’ve found that some lessons come in handy over and over again.

You’ll hear from many different voices in this guide, as we’ve purposefully attempted to curate a wide range of perspectives. The current founders, recession-era leaders and full-time investors who shared their thoughts don’t always agree with each other — and that’s intentional. It's more important than ever to take in different perspectives in search of the best advice for your company. From Zoom and Instacart to StubHub and OpenTable (and all of those startups caught somewhere between these extremes), it’s clear there isn’t a one-size-fits all answer for running a business these days.

We’ve organized this guide into eight parts, outlined below. Fair warning: While we’ve always had a penchant for long-form here on the Review, today’s effort is seriously long and perhaps not a read you can knock out over your morning coffee. Instead, we’re envisioning this as a resource to bookmark — one that you’ll hopefully return to over and over again as challenges crop up.

Also, be sure to check out this hub of resources we put together in Notion. It rounds up all of the recommended reads we share below, as well as our brand-new scenario planning template and list of curated job resources (both for candidates who are actively looking and companies that are still hiring).

PART 1: MAKING SENSE OF MACRO CONDITIONS AND MARKET SIGNALS

Let’s take a look at the broader context founders are operating in — and the case for why they might need to adopt a more conservative stance.

1. Brush up on your history as you make your bet.

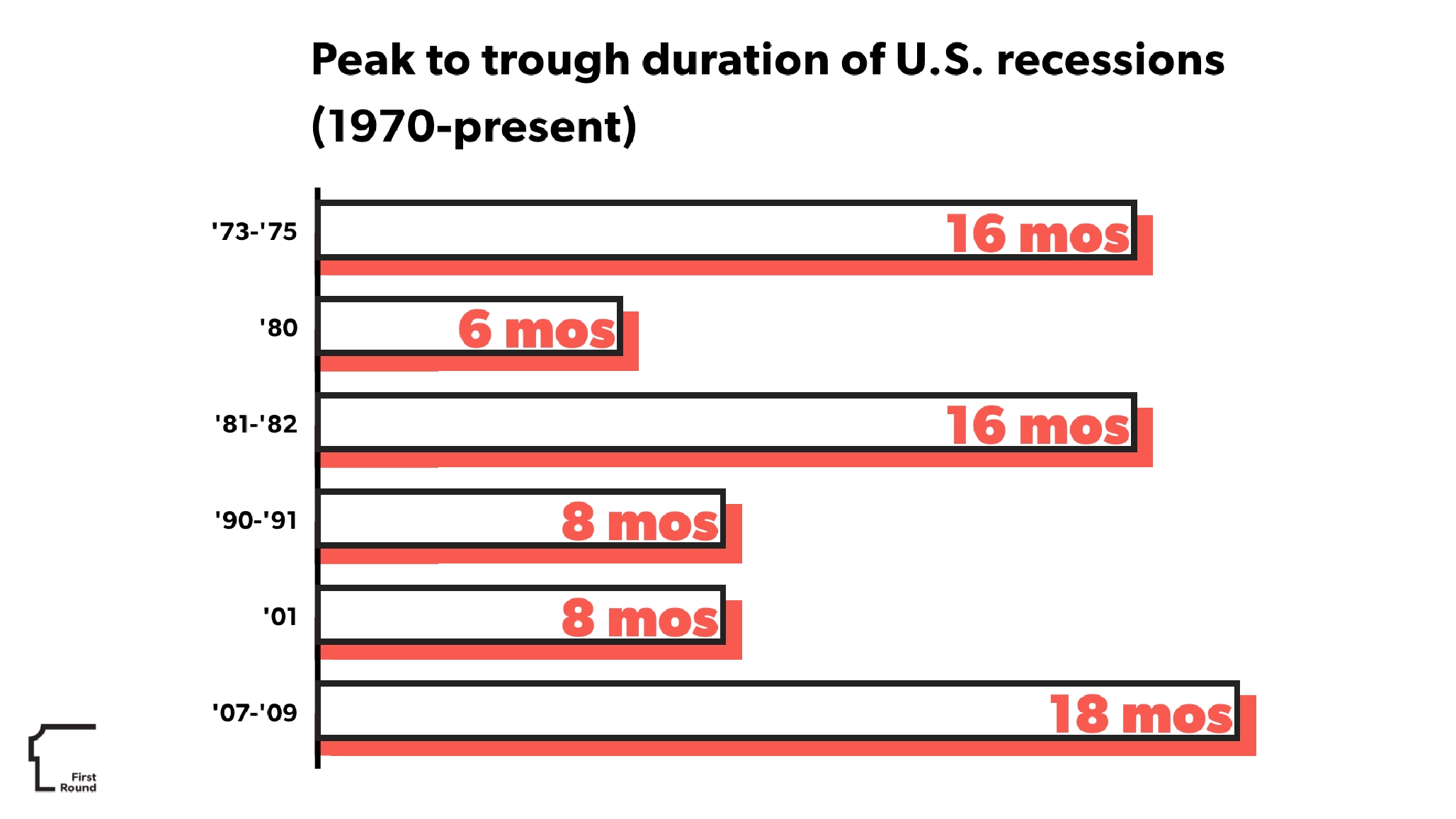

“Founders in their early 30s might have been in college during the Great Recession and everything’s been up and to the right ever since. So my first impulse is to make sure founders recognize that they are operating in a different environment than they were used to,” says Josh Kopelman, Founding Partner at First Round. “While there may be a fast recovery, I think it’s important to assess the probability of that occurring. If one was to look at the history of the largest recessions over the last 50 years, the average length is about 12 months. And that's not to recovery — that's just till we hit bottom. A quick recovery may be a possibility — but so is a long recession or even a depression. Know what you are betting your company on and force yourself to acknowledge it.”

His fellow partner at First Round, Bill Trenchard, agrees. “When budgets start coming down and people start maximizing profit over growth, it might be unbelievably hard to sell your product. There are multiple feedback loops of small business destruction, which can destroy a huge percentage of the jobs in the country, which in turn might destroy consumer spending, which could drive the whole economy down. To get more specific, nearly 50% of jobs in this country are with small businesses. Consumer spending drives our economy, and rising unemployement could lead to a massive drop in consumer spending.”

2. Watch out for false bottoms.

“I founded Half.com in 1999, and we ended up getting acquired and signing our term sheet right as the market was crashing. And then in 2008, I was a few years into building First Round and investing full-time,” says Josh Kopelman. “Across all of the downturns I’ve experienced, I’ve seen that people are tempted to underestimate the severity of that drop off in the beginning. There were a number of false bottoms, both in the dot-com era and in 2008. But because it would drop and then stabilize, people say, ‘Phew, okay, we're done now.’ And then 90 days later it would drop another +10%. So in the early days, it's hard to know the scale of what you're dealing with. The human mind is pretty great at taking in the stuff it wants to hear and drowning out the stuff it doesn't as ‘noise.’”

A key difference here is that we’re grappling with a pandemic. “In ‘08 we were trying to figure out when the banks would fail. Now, everyone's wondering, ‘Will the health system fail?’ And whereas government stimulus was the antidote before, now we're waiting for a literal antidote, in the form of a vaccine or antiviral approach.”

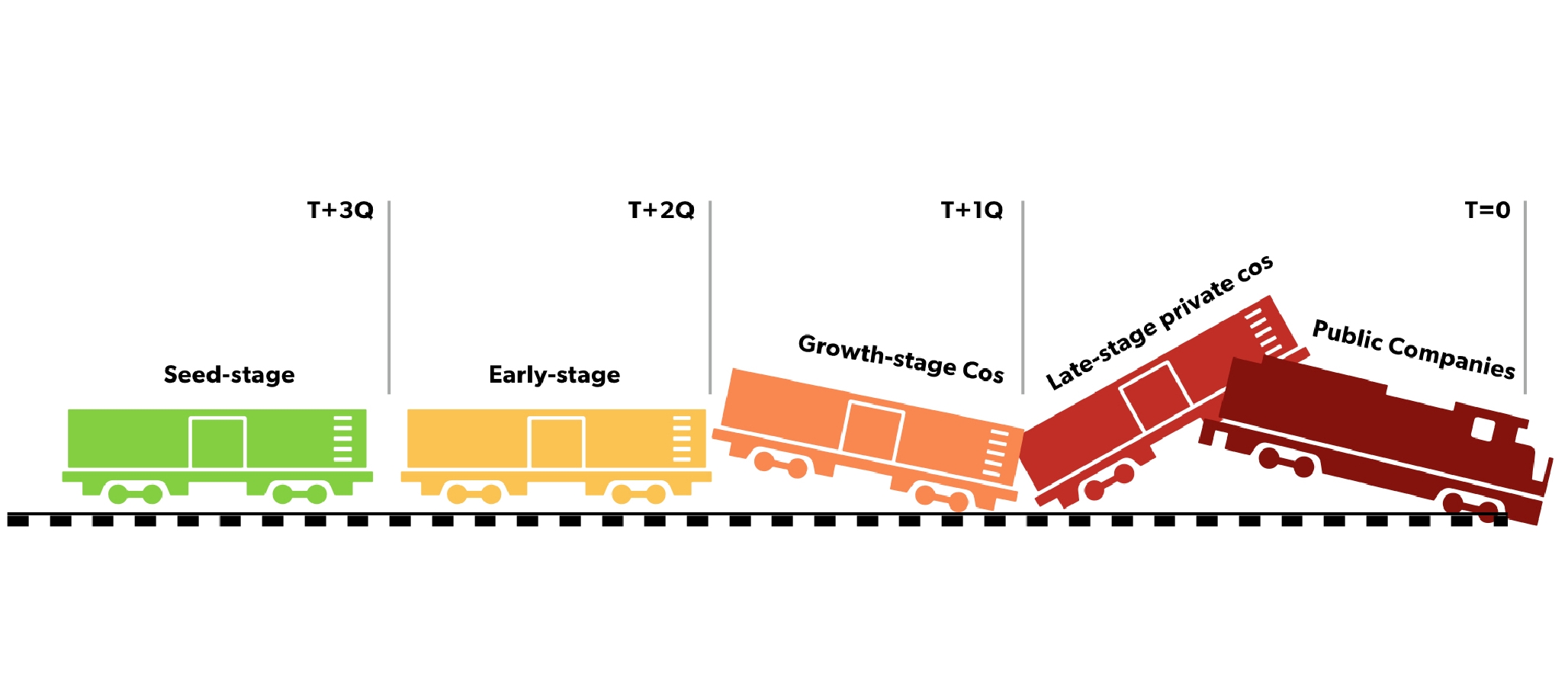

3. Look out for the locomotive effect.

Many seed- and early-stage venture-backed startups might think the turbulence in public markets doesn’t impact their business as sharply, given that any potential IPO is likely many years down the line. “While private markets do move slower — and a 20% dip in the stock market may not directly correspond to a startup’s valuation — there is a locomotive effect. As public markets are impacted, those changes cascade slowly throughout the chain, moving in (delayed) lockstep and sometimes playing out across several quarters,” says Trenchard. “Specifically, when public valuations shoot through the roof, Series A and B prices drift up. When late-stage and public companies hit serious turbulence, seed-stage startups need to take that into consideration as they think about their ability to raise follow-on rounds.”

In other words, it’s inextricably linked. This lesson is important to carry forward into other areas of your business as well. Though many startups in hard-hit industries are feeling the collision now, cyclical effects with customers also might be easy to dismiss.

“Early-stage founders may not be seeing any churn just yet,” says Trenchard. “They’re thinking, ‘We can continue selling to customers at home, no big deal, things will bounce back.’ But just because you believe you’re firmly in an unaffected market, that doesn’t mean you will continue to be in the future. Things can change, fast.”

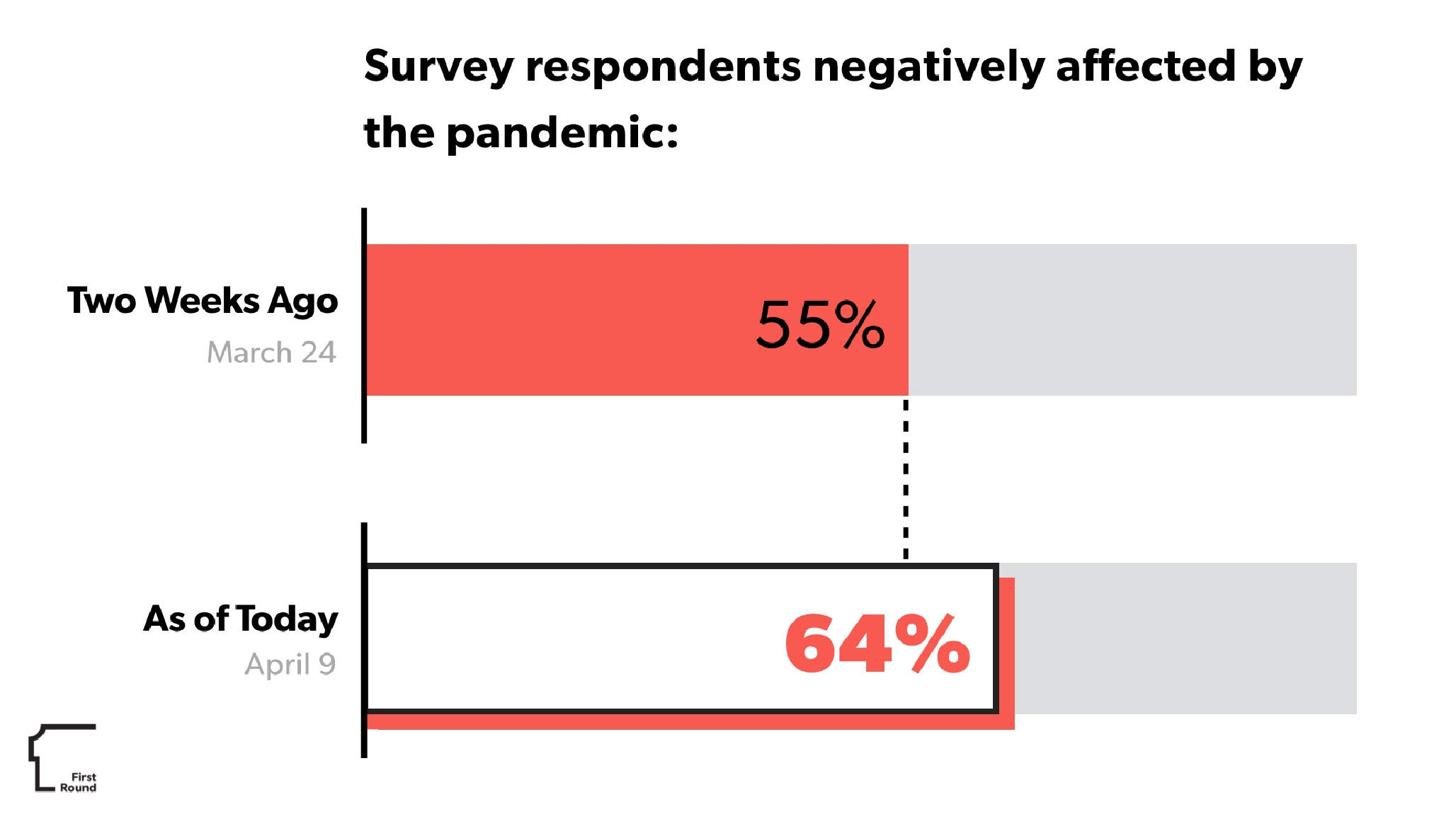

To illustrate just how quickly the ground game is changing, we embarked on a new effort (inspired by our State of Startups report) to create a 2020 pulse survey on how venture-backed founders are planning to navigate this crisis. We will be sharing a few snippets of initial findings here in this guide, starting with this one: In just two weeks, we found that the percentage of survey respondents who reported being negatively affected by the pandemic rose from 55% to 64%. (We plan to continue these pulse surveys to track how founder sentiment changes rapidly over time, so more to come.)

“When a recession starts, nobody knows when it will end or how deep it will cut. We won’t know for a while, but instead of waiting to find out, brace for impact by assuming that these conditions will broadly and harshly impact your customers,” says Mark Bartels, the current CFO of Invoice2Go and previous CFO of StumbleUpon.

Current Andreessen Horowitz General Partner (and former CEO and co-founder of TrialPay) Alex Rampell made a related point on unseen effects: “Lots of companies think their business is counter-cyclical. At TrialPay, we thought that no business could be more counter-cyclical than one giving away stuff for free, right? Well, that was true on the customer demand side, but the cascading effects are sometimes hard to prognosticate, so don't be arrogant,” he says.

“As an example, TrialPay was the number one source of Washington Mutual new checking account customers in 2008. Haven't heard of Washington Mutual? That's because it went insolvent. We were their best channel. They made money on every customer we sent them, but the macro-environment killed them.”

Additional resources on the macro-environment:

- Foursquare analyzed foot traffic patterns: How COVID-19 is Influencing Real-World Behaviors

- JPMorgan Chase Institute’s Cash is King report researched the financial lives of 600,000 small businesses in 2016.

- Womply Slide Deck: 2020 Economic Apocalypse: The Effect On America's Small Businesses

- London Business School Lecture: The economics of a pandemic: the case of Covid-19

- Divinations newsletter: Understanding the Covid-19 Recession — What happens when an economy holds its breath?

PART 2: THE CASE FOR RESPONDING QUICKLY AND THINKING THROUGH SCENARIOS

Given these broader conditions, how should founders respond? From springing into action to make conservative cuts to taking a more cautious “wait and see” approach, there are many different paths to consider. Here’s the general consensus we found: Move quickly, but prudently. A “business as usual” response with no alterations to your pre-pandemic plans is probably not the right approach, nor is an impulsive reflex to drastically slash. This is where the importance of scenario planning comes into play.

Founders tend to be an optimistic bunch, so it’s key to check your biases and challenge your thinking throughout this process. Stay open-minded about the broad range of possibilities and develop several plans for different outcomes so you aren’t left scrambling later. Some folks who shared advice with us disagree on how much you’ll need to change your plan or how aggressively you should pursue those changes — but all agree that you need to get planning.

1. Account for the widening aperture.

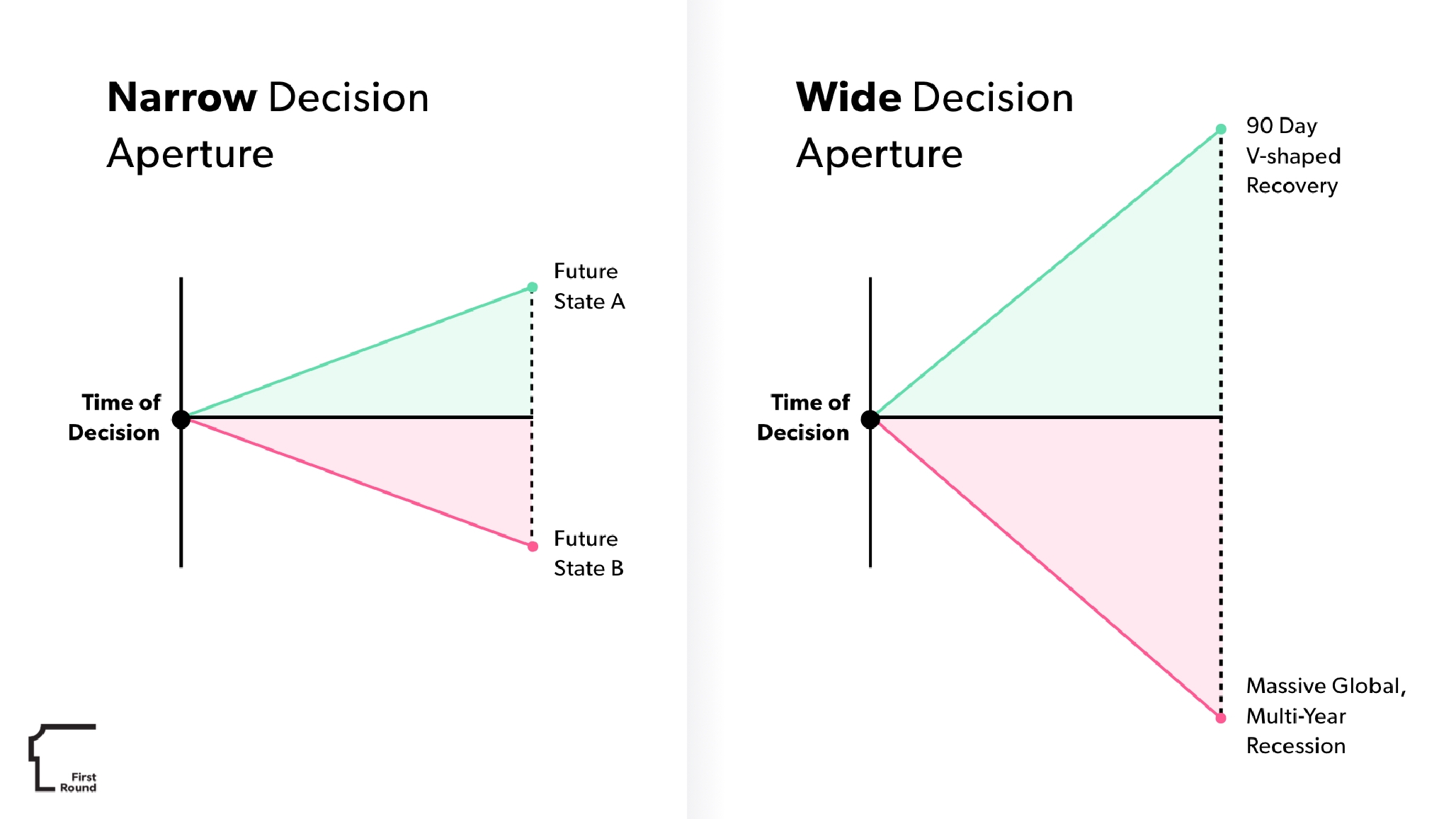

Day in and day out, CEOs are tasked with making decisions about the future based on the information available at present. In other words, you’re placing bets on how to allocate your resources. “The job of a founder is always to predict the future. When you're starting a company, it’s because you have a prediction of how the world could be different,” says First Round’s Josh Kopelman.

Under normal conditions, founders assess capital markets, customer demand, competition, distribution and sales velocity to make those bets, assessing the decision aperture between possible future states. Typically, more time yields more data, a smaller aperture and higher accuracy in decision-making. But in black swan conditions, that aperture is wider than ever. “There’s so much variance. You could be looking at a 90-day recovery, six months of choppiness and then back to normal, or a massive global, multi-year recession,” says Kopelman.

Here’s a quick overview of those potential alphabet-based scenarios you’ve likely seen referenced before:

- V-shaped recovery: A sharp, precipitous drop, followed by a swift rebound as the economy recovers. The 1953 U.S. recession is an oft-cited example.

- U-shaped recovery: The bottom is a less-clearly defined curve, as opposed to a pointy trough. (The former chief economist of the IMF once compared it to a bathtub). Growth does recover, but it takes longer than planned. Think of the 1973-1975 U.S. recession.

- L-shaped recovery: A severe recession or depression, where even after recovery, the growth rate can still be lower. Japan’s “lost decade” in the 1990s illustrates this shape.

- As this article from Bloomberg points out, economists theorize that other shapes are possible as well.

2. Beware of the dangers of delay and doing nothing.

“When the action you need to take is painful, like austerity measures, there’s a cognitive bias toward delaying until you’re very certain the actions are necessary. The issue is that in a case where the probability of the worst-case outcome realizing increases with time, by the time you are certain about the need to act, it may be too late,” says Kopelman. “In this case, the risk of ruin increases with time. Every day you don't reduce your burn rate is a day that narrows your chances of being able to ride this out if the worst comes to pass.”

People generally prefer to delay painful choices, are overly optimistic about their own fundraising chances and wait far too long to gather certainty that those choices are necessary.

“Oftentimes, when founders opt to do nothing for now, they think they aren’t deciding just yet. But they are. This is omission bias at work. Changing things feels like a decision, whereas staying the course doesn't. But they are both decisions and need to be viewed as such. Because if you do nothing, you're basically saying the landscape hasn't changed for you. And while that may be the case for some companies — an early-stage startup that had planned to spend the next year writing code, for example — most startups are seeing a change of some sort,” he says. “I’m informed here by my previous experiences with economic contractions. The companies and the founders that really understood the scope of possible outcomes and put together a scenario plan for the worst outcome — while hoping that the worst outcome didn’t materialize — were the ones that survived. The ones that waited too long struggled.”

Doing nothing is a decision. It’s the same as actively choosing to stay on the same path. And most founders don't realize that. If the winds are changing, a smart sailor will adjust their sails.

Gina Bianchini agrees. (She’s the current CEO and founder of Mighty Networks, and from 2004 to 2010 was the CEO of Ning, which she co-founded with Marc Andreessen). “Many founders I’ve talked to recently have said variations of ‘It’s only a couple weeks, we’ll be able to wait it out,’ or ‘I just need to move. We'll show more empathy in our outbound sales sequence, and things will pick up.’ The odds of that all being true for everyone may be low,” she says. “I understand the impulse to project an image of having everything together. People are scared, and things are uncertain. Plus, we can still remember ‘normal’ from three weeks ago, so there’s a lag-time as well. But if you wait too long to act, there’s no amount of optimism or tactical shifts that will save you — everything else might be rearranging deck chairs on the Titanic.”

3. Pick up the tempo.

The speed of your company’s decision-making has always been critical. Couple a fast-changing environment with our tendency to kick the can down the road or be overly optimistic, and it stands to reason that a “wait and see” stance might not be the best approach here.

“Re-work the plan. Immediately. Not in a quarter. Not in a few weeks,” says Simon Khalaf, the current SVP and GM for Messaging at Twilio. (Back in 2008, he was the President and CEO of Flurry Analytics.) In other words, you shouldn’t be operating at the same tempo as you were 90 days ago, but it can be tough to go from planning quarterly to planning weekly. “We are at a time of incredible uncertainty. Changes that might have happened in a year are happening in a week. Macro shifts are happening fast, but the micro-level of what’s happening in your business — signed contracts, churn and so on — still may be slow,” says First Round’s Josh Kopelman.

Here’s why that’s particularly challenging for founders: “Most CEOs also have a tough time thinking about the macro picture. They're so focused on the micro lens of their company, their employees and their customers — that's enough to already have on your cognitive plate. It’s not a muscle they’re used to exercising,” says First Round’s Bill Trenchard. “But the best founders are resetting immediately. They’re saying, ‘Oh my God, I’ve really got to think about the bigger picture and I don't do this normally. How do I get smart on that? Who do I talk to? What do I plan for?’ And then they do all of that scenario planning work, pick what they think is the most likely outcome and then start implementing to take decisive action.”

PART 3: THE NUTS & BOLTS OF SCENARIO PLANNING —OUR 5-STEP FRAMEWORK AND TEMPLATE

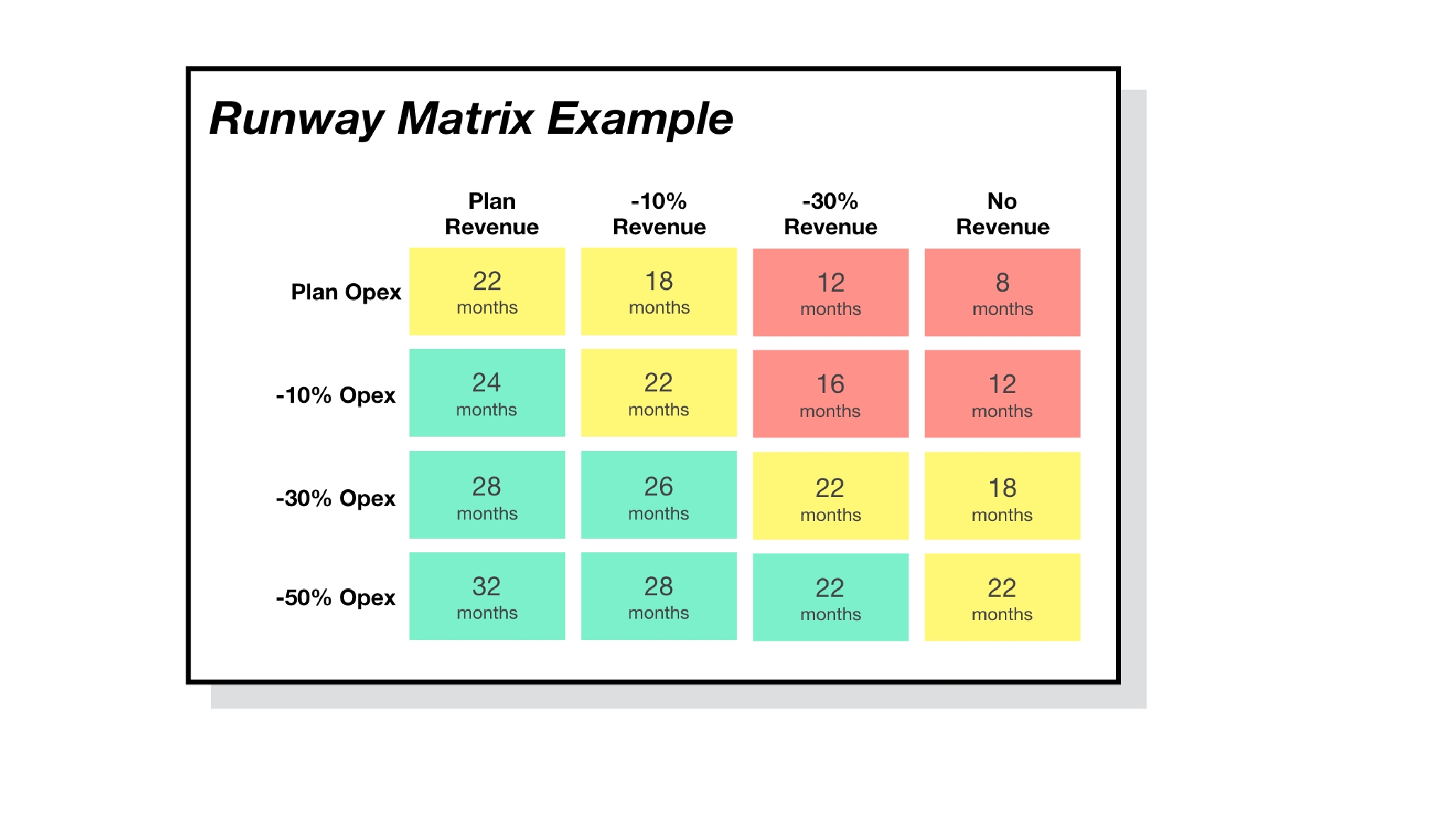

But how exactly do you prepare for that decisive response to changing conditions? At a minimum, it’s crucial to get a firm handle on your company’s cash position and runway. Borrowing from our friends at Sequoia, we recommend starting with a simple matrix. We advise securing at least 24 months of runway (green cells), and have advice throughout this guide on how to get there.

If you’ve already done this work and are looking to go deeper, below we outline the 5-step framework we recommend for more advanced scenario planning.

Why you need a scenario planning framework:

“Right now, as a leader, your job is to imagine how your company needs to be different. What are the different future scenarios for the country, for the economy and for your company? And how does your company both survive and thrive in that time? You need a framework for how to plan,” says Kopelman. “The essentials are converting your observations and assumptions into possible scenarios and then outlining how you would adjust your current, pre-COVID operating plan to respond to those scenarios.”

It's better to have a plan that gives you the best chance of survival under a variety of recovery scenarios. Plan for the worst-case recovery — but hope for and position yourself for the best-case recovery.

This scenario planning exercise is about thinking through your options, he underlines. “It’s scary when founders have a reflexive impulse to just cut 40% right off the bat. Maybe that's the right answer. Or maybe it's a 10% cut. Or perhaps cutting isn’t the right move at all. Let's understand the impacts of different scenarios that could unfold first,” Kopelman says. “A good plan might say, ‘Let's wait 30 days and if the following things happen, we'll do X, and if the following things happen, we'll do Y.’”

First Round partners have been leaning on these principles as we hold multiple working sessions with all of our founders. But we wanted to dive even deeper and share these resources beyond a high-touch, 1:1 approach, so we've worked to boil it down into a repeatable process for all to use.

If you’re curious how this approach could work in practice, our friends at Notion helped us set up this Scenario Response Planner template — which includes example responses for a fictional corporate catering service. Duplicate our template to start working on your own company’s plans.

Step 1: Identify your key uncertainties.

To start this process, identify the 6-10 key uncertainties introduced by COVID-19 for the next year to inform your planning.

Will public health response effectively and rapidly control the virus spread? Will economic policy interventions prevent widespread small business closures? Will social distancing policies have a lasting effect on your customer’s buying behavior? Everyone’s list will be different. Focus on what you think will have the most profound impact on your company's prospects and strategies and be sure to include a range, from macroeconomic and epidemiological uncertainties to those concerning your market, customers and other stakeholders.

Step 2: Bucket them into scenarios.

Using combinations of outcomes from your uncertainties list, create three (or more) scenarios: a best case, a worst case, and one that splits the difference. Think carefully about how you assemble each scenario, so each includes a plausible combination of outcomes and captures a useful business case. You might do that based on the potential letter-shaped economic recoveries we discussed earlier. Patrick O'Shaughnessy offers another helpful trio-based metaphor: blizzard, winter or ice age.

To bring each of them to life, we suggest giving each of your scenarios a name and narrative, so they feel less abstract and more tailored to your company’s specific situation. For our fictional corporate catering service, we chose:

- No Return (Worst Case): Workers don’t fully return to offices until 2021, restaurant closures are widespread, and demand for corporate catering plummets.

- Soft Rebound (Middle Case): Workers don’t fully return to offices until fall 2020, restaurant closures are significant but contained, and demand for corporate catering is present but reduced.

- Old Normal (Best Case): Workers return to offices in summer 2020, widespread restaurant closures are prevented, and demand for corporate catering is largely unaffected.

See the more detailed assumptions that went into these fictional scenarios over in our Notion template.

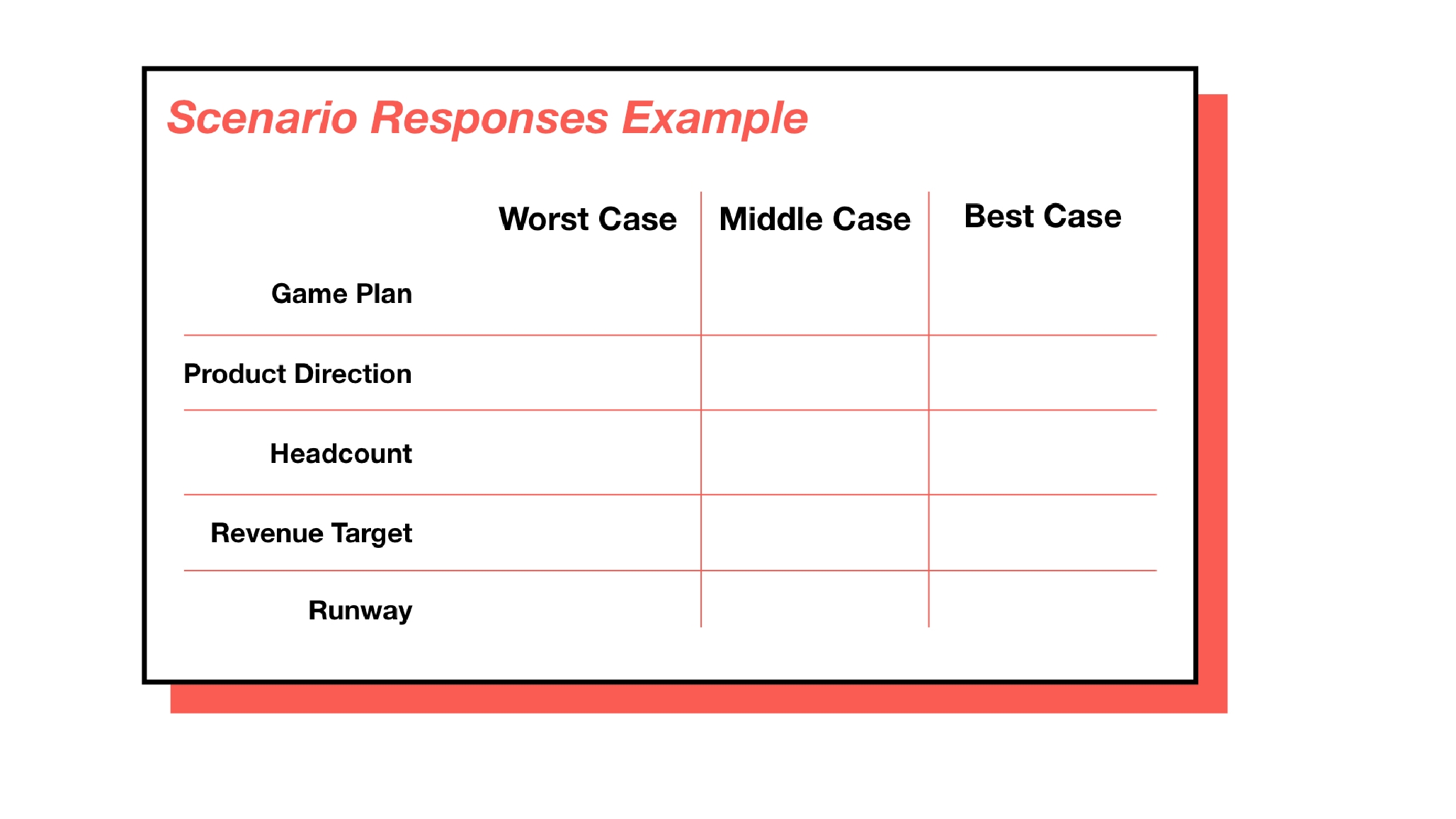

Step 3: Craft responses to each.

If your scenarios describe where the world might be heading, your responses answer the question, “Now what?” Regardless of which future arrives, one thing’s clear — it will favor the companies that moved fast.

Do so by generating responses for each that can drive specific decisions and actions at a more granular level. Use something like the table below to think through how your overall business game plan will change scenario-by-scenario. Break down the steps you’ll take in terms of revenue targets, product direction, headcount — and the runway and burn rate you’ll see as a result.

See the example we filled out for our fictional startup in more detail here.

Step 4: Look for triggers points.

We believe General Dwight Eisenhower was spot on when he noted that it’s the planning process — not the actual plans themselves — that is indispensable. That said, we find these scenario plans are made more useful (and less abstract) when you’re monitoring for concrete internal and macro triggers that will help you decide which path to choose. Here are some sample indicators to consider:

- Macro: Extensions or changes to shelter-in-place policies, job loss trends, small business closure rate, and so on.

- Internal: Customer churn stabilizing or dropping, pick up (or drought) in inbound sales leads, and so on.

You can augment your scenario responses by adding specific trigger points for each. (For example, restaurant closures beating estimates, job losses start to stabilize and a pick up in inbound sales leads could all fall under your best case or “return to normal scenario.”)

Step 5: Revisit, revise and repeat.

Every two to four weeks, archive your old uncertainties, scenarios and responses and copy/paste the builder template into a fresh version. Use these rewrites as a chance to think hard about what's changed, whether your scenarios are still realistic and to alter your course of action in response.

“If today is April 9, then you’re creating version 1.0 today, and then you’ll create version 1.1 on May 9, highlighting what changed in your assumptions and in the world. And then in June, you create 1.2, and so on,” First Round’s Josh Kopelman recommends.

Here’s why this matters: “Once people decide on a model, there’s a risk of getting entrenched. Try to come out of this planning process with a list of things that might be true of the world and a list of signals that would tell you that a V, U or L shaped recovery was occurring," he says. "Write those down and then be vigilant in looking for those signals. Don't get trapped in your own initial assumptions. This will make you more agile and flexible as the world starts to send you signals, which is especially important when there is a lot of uncertainty.”

Writing out your assumptions in a living doc forces you to recognize what's changing.

First Round’s Bill Trenchard agrees. “One founder I’m working with is planning for a middle scenario recession but hedging that bet. Because he has a round in the bank, he’s keeping an extra salesperson in case he’s wrong and things do come back quickly, so he doesn’t lose out on the onboarding and ramp time. This founder is sending almost weekly updates to the board, with what he’s seeing, what he’s doing and how he’s changing his plan now that we have three to four weeks of data.”

Additional resources on scenario planning:

- Dan Hockenmaier’s post on how to scenario plan for COVID-19

- Sequoia’s Matrix template for COVID-19

- HBR 2009 article: Seize Advantage in a Downturn

- Boston Consulting Group’s slides on COVID-19 dynamics and implications

- Howard Marks: Memo to Oaktree Clients

PART 4: BROADER THOUGHTS ON EXTENDING YOUR RUNWAY

With scenarios in place, if your planning outcomes dictate finding ways to extend your runway, here are some approaches to consider. We’ll start with some general thoughts and different perspectives on what’s most important to prioritize. Then in the follow-on sections, we’ll dive deeper into the specifics of cutting costs (pausing hiring, cutting expenses, reducing headcount) and bringing in more capital (customer funding, fundraising, venture debt).

The advice we’re sharing with First Round companies on runway:

Think of your cash as an insurance policy. Insurance was made for unexpected events — and you hope you never have to use it. In other words, you hope your house doesn't burn down, but you buy the fire insurance in case it does. Similarly, if the recovery is quicker than you expected, that doesn't make the decision to have a lot of cash on hand wrong. Don’t be afraid that you’re overreacting because you hope it turns out you won’t need the extra runway. The more uncertainty, the more you need the insurance that you wish you won't need.

Underwrite yourself with +24 months of runway, if you can. If you raised more recently, try to bank 36 months to give yourself even more flexibility.

One of the primary jobs of a CEO is to manage existential threats. And the number one existential threat right now is running out of capital.

If you think about your runway in those terms, then chances are you’ll need to get more conservative with your projections. This is particularly true given the sea of unknowns ahead. You might find certain levers that used to be efficient get turned upside down, such as a particular sales motion that’s no longer working. Another reason it pays to play it safe here? The end-to-end fundraising process has just gotten harder — and therefore longer.

More fundamentally, you need to refactor all of your assumptions. “When you raise money as a founder, that money has a job to do. You were going to use it to build the products, to prove out tech or to figure out go-to-market,” says First Round’s Josh Kopelman.

“Here’s what I’m asking all the founders I work with: You made a bet on an amount of time and an amount of runway to do a job, but now, what if you assume that 2020 is a lost year? How does that change things? If you were planning on selling, implementing, deploying or growing, and if you instead assume 2020 is done, what does your runway look like? What does your business look like? Do you have enough runway to then do the job you wanted to do and still have time?”

Advice from recession-era founders on runway:

Here’s a quick hit list of tips from several founders who felt the pain of a shortening runway firsthand in previous downturns:

- Get cash early and make it last. “$1 today is much more valuable than $1 in two years,” says Alex Rampell (current GP at A16Z, previous CEO/co-founder of TrialPay). “Give discounts for early payments. Survival is everything. Make the money last, last, last. With TrialPay, we didn't raise a round for another three years. Had we needed to, it would have been very difficult, especially given that valuations tend to reset (a ‘re-rating’) after these massive bumps.”

- Get capital by not needing it. “I was meeting with some founders the other day, and I asked them about their cash flow positive scenario. They didn’t have one. Now more than ever, it’s important to control your own destiny,” says Gina Bianchini (of Mighty Networks and Ning). “You know that investors are going to care about being cash flow positive in a way that they didn't two months ago. Who's going to be able to raise the most amount of money? The people that are already cash flow positive, or have a path to it. Look at Notion raising $50 million last week. Especially in a downturn, people want to give money to companies that don’t need the money.”

- Think about future impact, not just getting through today. “Take the steps you think you should do anyway, even if we have a quick recovery. Use this opportunity to take those actions to make the company stronger in all circumstances,” advises Ken Goldman, former CFO of Yahoo and Fortinet. Seth Sternberg (who was building Meebo in 2008) offers a similar piece of counsel: “Make these pivots durable. Think about what you can uniquely do in a time like this that has a lasting impact beyond the moment. Do those things first. Something that only helps right now is less good than something that'll help your business once we get back to normal.”

- Don’t take anything off the table. One more from Sternberg: “In times like these, you can literally reexamine all assumptions. There's a free pass to do things that would normally be taboo or signs of a failing company. So reexamine everything you do. Pricing. Salaries. Team structures. If you haven't cut anything, you probably haven't reexamined enough,” he says.

- Remember this feeling. “The lessons I learned building TechForward in the last downturn have definitely stayed with me,” says Jade Van Doren. “Most recently, when I took the CEO role at AllTrails in 2015, the company had minimal revenue and a six-figure per month burn rate. Rather than focusing on raising money, we dove into improving the quality of the product, the associated trail data and optimizing the sales funnel. Within six months, the business had turned cash flow positive, and we were able to grow organically without additional capital into a $75M+ private equity sale in 2018 — with just 14 employees. Perhaps because the events of 2008 burned financial discipline into me, I now prefer running and investing in leaner, more product-led-growth companies, even in economic environments in which others might have turned to dollar-led growth.”

- Extend your runway — but make sure it leads somewhere. “I do support rational budget cuts. Conserving cash is a wonderful thing. But the goal needs to be more than just ‘X more months of burn,’” says Oren Michels, the CEO and co-founder of Mashery during the Great Recession (which was later acquired by Intel and then TIBCO). “If you cut back significantly now, you might get to a place where you can squeeze out a few more months of burn. But to what end? On the other side, you’ll be treading water, trying to ramp back up for at least as many months as you saved in burn. There’s something to be said for thinking through scenarios, but waiting to pull the trigger. You can make cuts pretty quickly — it’s the undoing cuts and restarting product development or go-to-market that takes way longer.”

Additional resources on runway:

- Airbase panel recap on Navigating Uncertainty: Extending Your Runway

- First Round Review article: How This Founder Turned Slow Burn Rate into a Big Exit

- Auren Hoffman’s post: Here’s How Your Start-Up Can Not Only Survive the Recession But Actually Come Out Stronger

- Twitter thread from Sahil Lavingia, founder and CEO of Gumroad, about getting to profitability

PART 5: HOW TO REDUCE BURN — STRATEGIES FOR CUTTING COSTS

If you’ve committed to the path of dramatically reducing your burn rate, we’ve gathered advice for two common paths: cutting expenses and reducing headcount.

1. Cut expenses:

Try to bring down the burden of rent.

Outside of your team’s compensation, rent is likely one of the most significant line items in your budget. While your lawyer should review your contracts first, you may to want to consider these strategies:

- Rent abatement: Most landlords have developed leases that — when they contain force majeure clauses — still require the payment of rent during emergencies. The best approach to obtaining rent relief is a direct negotiation with your landlord — before they get inundated with requests. Many are open to restructuring a lease to provide for short-term relief. Try negotiating a temporary or permanent discount to your lease rates, or getting a discount in the form of a credit. (As an example, offer to stay current on your payment for the next three months, in exchange for two months tacked on for free at the end of your lease.) In deals known as blend and extend, some landlords are agreeing to no rent or lower rent for a period of time, with the foregone rent being added back and amortized over the monthly payments for the remainder of the lease. In many cases, those deals involve an extension of the lease.

- Downsizing: This is applicable particularly for companies who are in modular spaces (WeWork, Knotel, etc.) and can consolidate the space they need. Many of us may be working from home for the next 12-18 months, at least part of the time, in accordance with ongoing quarantines. Do you really need that office space? Can you get by with shared space, part-time space, a WeWork membership?

Clean up by running through this thought experiment.

“Ken Goldman recently shared that this is a great opportunity to tidy things up,” says First Round partner Bill Trenchard. “Since we haven’t been in an era of belt-tightening, many companies have probably gotten a little sloppy, racking up some expenses they don’t absolutely need. This is the time to clean it up. One startup I know cut 25% of their expenses — without cutting a single head. That means you're taking actions like getting rid of a bunch of perks that no one ever used. That’s a good first step that makes companies leaner and meaner.”

Here’s a thought experiment for every founder: Imagine it’s 18 months from now. Your company has run out of cash. What are the top five things you wish you hadn't spent money on?

Tactics for cutting expenses, recommended by current CEOs in the First Round community:

Here’s a handful of other tactical ideas, sourced from the First Round community:

- Be very careful about marketing spend, specifically on the enterprise side. Advertising costs may be cheaper, but you don’t know how the funnel will convert yet in this new environment.

- Cancel credit cards and issue new ones so you can zero out expenses quickly. This will end all recurring charges — and force the company to explicitly re-subscribe to all essential services. (Downside here is potentially losing important infrastructure that’s tied to cards, so be sure to do a sweep for that first.)

- Ask your team to look for savings and give them a percentage of everything that the company saved as a bonus. There is an amazing amount of money that can be saved if you go line by line through every expense you have. In a counterintuitive way, it all adds up.

- Look to try to lower the absolute cost of software subscriptions and eliminate seats or licenses that aren't mission-critical.

- Reconsider the services you have on retainers, such as PR firms.

2. Take a serious look at headcount:

Once founders have moved beyond reducing expenses and potentially rent, headcount is the next bucket to examine closely. Of course, this isn’t about line-items in a spreadsheet. Our single biggest piece of advice is to remember that these decisions will have a profound impact for the humans on your team. Explore all your options before diving straight into layoffs.

Before we proceed: If you’ve been affected by layoffs personally, check out these resources we've curated here. Several First Round-backed startups are still hiring, and our talent team is standing by, ready to help get you in front of companies in our community. If you work at a company that’s still actively hiring and would like to get in touch with newly available candidates, we’ve also collected some helpful resources for you here.

Start by pausing hiring.

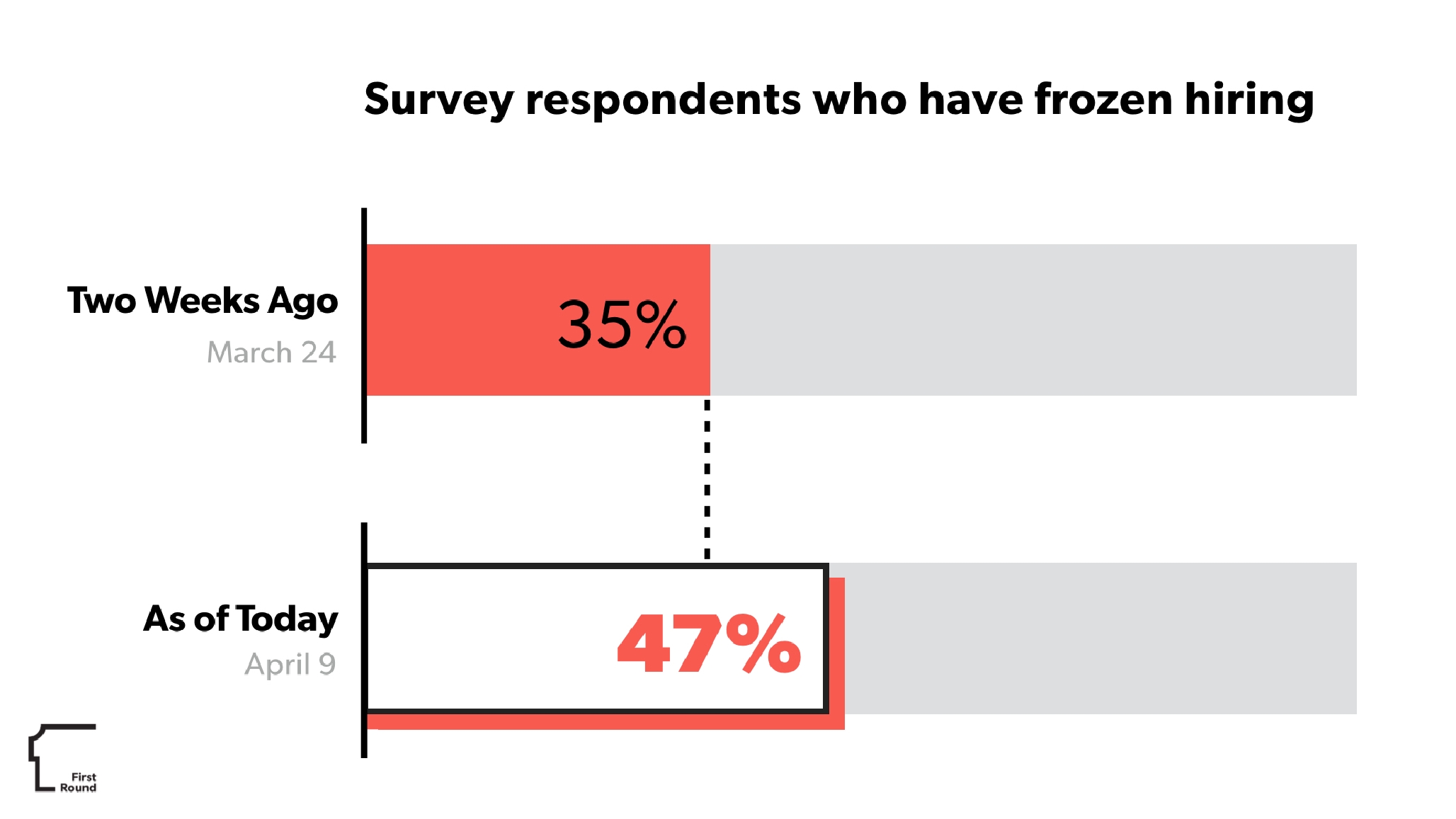

What other founders are currently thinking: Many startups have already put this in motion. Two weeks ago, 35% of founders we surveyed reported they’d frozen hiring. As of April 9, that had risen to 47%.

If you have an aggressive hiring plan, especially in sales and marketing, consider pausing or reducing if you haven’t yet done so. Unless you’re in the segment of companies that will benefit from the current state of affairs, companies and individuals will be buying less. You very likely may have all the team you need to accomplish a reduced revenue plan for the year.

Consider reducing comp.

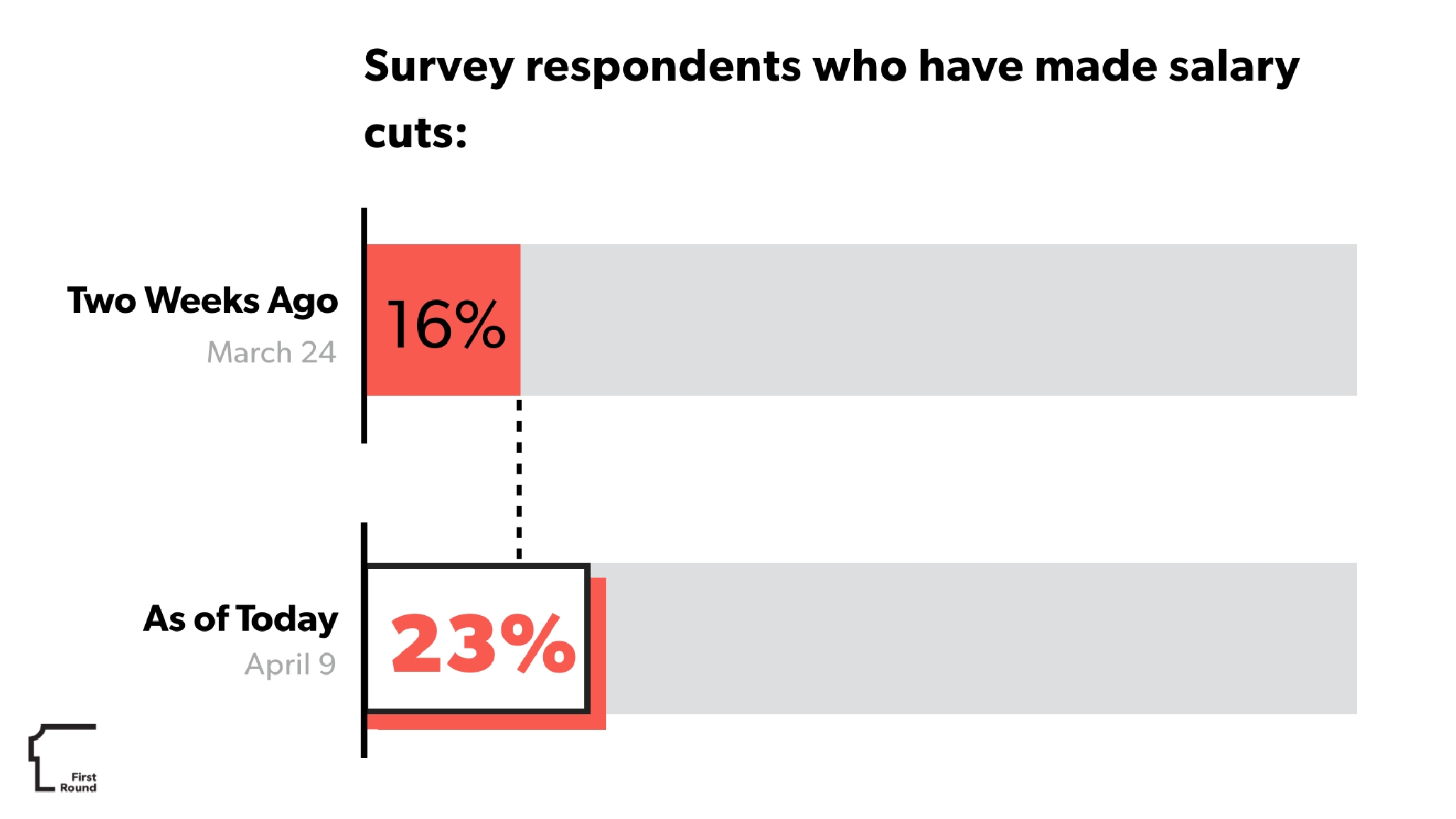

What other founders are currently thinking: Back on March 24, only 16% of founders surveyed reported they’d made salary cuts. As of April 9, that had risen to 23%.

If you haven’t yet, consider cutting executive salary as a way to show your team that everyone is feeling the pain. You may be able to pay it back in the future when the balance sheet is stronger. You can also think about increasing equity as you look to decrease cash spend. Reducing 401k matching and forgoing bonuses for the rest of the year is also an option.

However, one CEO we know pushed back against this idea: “I don’t think salary reductions are the right path. No matter what they say, people never feel good about it, they’re always looking to get back to normal and be made whole, which is understandable. Don’t promise it’s ever coming back, that’ll stick in their mind and you’ll be boxed in.”

Think carefully about a reduction in force.

When layoffs are announced, it will be the hardest day in any young startup’s history. It’s incredibly difficult to say goodbye to the exceptional individuals you handpicked and hired, the ones who’ve helped you get the company to where it is — and of course, unimaginably distressing for those who are affected. It’s also important to recognize that letting team members go today, in April 2020, is fundamentally different from a layoff under any other circumstances, given uncertain future job prospects.

As First Round’s Bill Trenchard notes, there’s also the challenge of taking hard questions on this topic. “‘Is my job safe? Are you going to lay me off?’ Unfortunately, no one can promise absolutely not. That’s not true for any situation, in good times or in bad. But you have to know how to deliver that message. You can say, ‘We don't expect that. Here's the data we see. Here's how we're looking at it. And if there’s any change, you'll be the first to know. We're going to do everything we can not to make it a surprise for anybody,’” he says. “It’s like this tiger is lurking behind you — folks want to know that they’re not going to get jumped from behind.”

If you do decide on layoffs, try to ensure you don’t need to do another round. If possible, you only want to go to that well once, as each round tends to erode morale. Also, consider that furloughing is an option. An employee furlough is a mandatory suspension from work without pay. It may or may not include the continuation of health benefits — if you want to continue them, you need to make sure the terms of your plan allow for that. Furloughed employees are typically entitled to claim unemployment and they are banned from doing any work on behalf of their employer. As a result, furloughed employees typically have their access to work accounts and devices revoked to prevent well-meaning employees from breaking the law and triggering a payment obligation.

Founders: Before conducting a large layoff or any furlough, you'd be well served to speak with your employment counsel as there are a number of issues involved.

What other founders are currently thinking on layoffs:

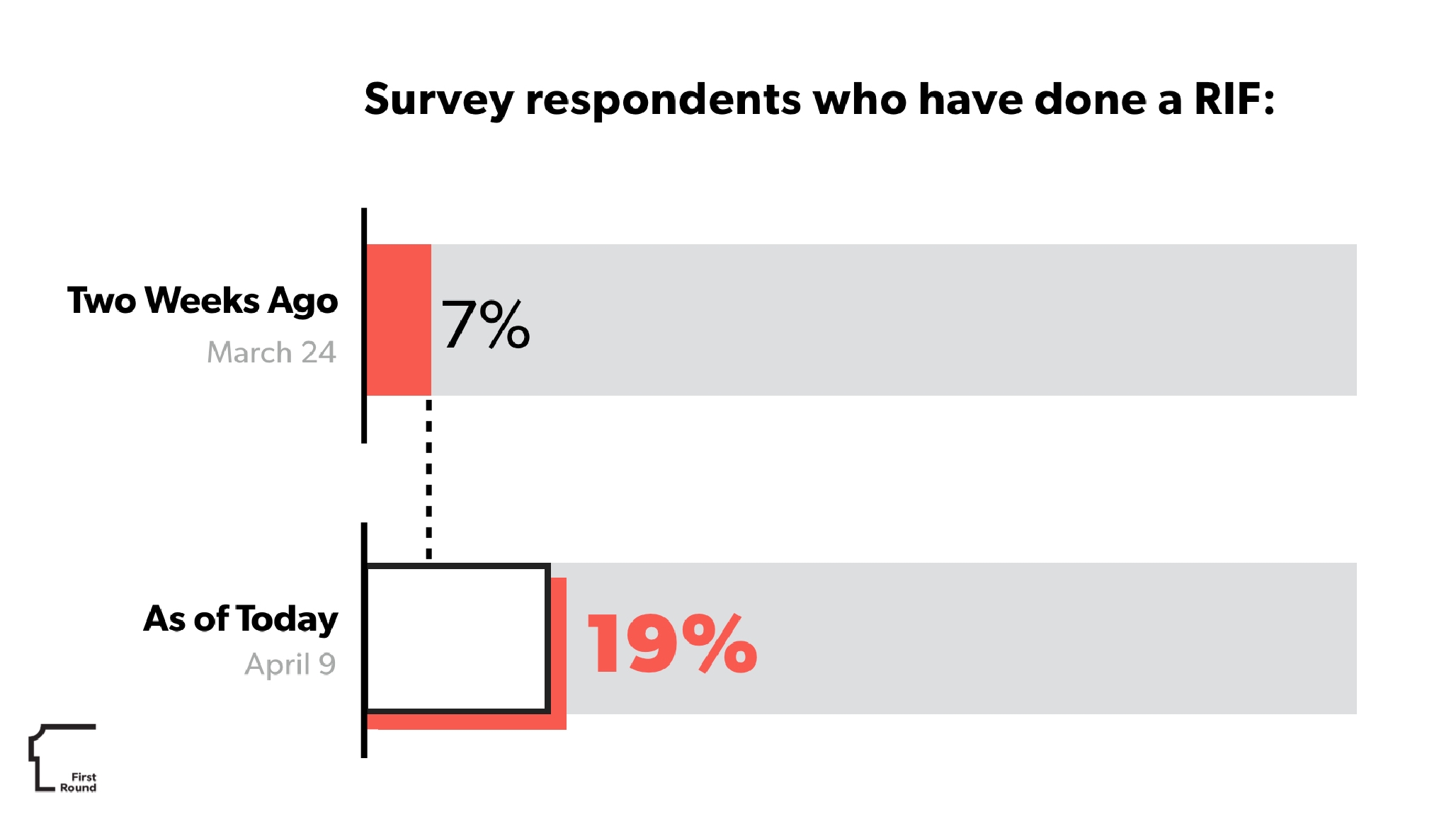

Two weeks ago, 7% of founders surveyed reported they’d made a reduction in force. As of April 9, that had risen to 19%.

Advice from recession-era founders on layoffs:

- Measure twice, cut once. “First, think hard about if you want to cut or not. If you’re in a market where things are still unclear, I don't think the answer is to layoff your entire team right away,” says Gina Bianchini, CEO of Mighty Networks. “And before you cut, spend at least a couple of days looking at revenue before you start eyeing headcount. How else could we market this? Who do we know? Then look at how we could reconstruct or reconfigure our team so that we’re not burning as much cash?” she says. “After all that, if you’re in a market that’s not accelerating and you are going to cut, cut deep. I don’t say that to be uncaring. It’s actually uncaring to put a team in a situation where the founder isn’t honest about where you’re sitting in the market. There’s no shame in being in a market that disappeared overnight. And that goes both ways — it’s not personal if things are working either. But as founders, we often feel, ‘I recruited this person, I’m their leader and I’ve let them down.’ You haven’t if your market changed overnight,” she says.

- Consider your stage and bring every bit of EQ. Matt Sanchez, who built VideoEgg (now SAY Media) in the last downturn, thinks layoffs can be necessary in many cases in this environment. “For companies with no revenue, or early in achieving product/market fit, cutting deep and quickly to manage burn is absolutely the way to go, even if it's scary to take that step. For companies with meaningful revenue, cut to a conservatively-forecasted run rate,” he says. “Do everything you can to be rational and fact-based in your decision-making, but bring every bit of EQ you can to your leadership and execute with compassion.”

- Avoid across the board cuts. When it comes to deciding where to cut, Simon Khalaf, former CEO of Flurry Analytics, recommends that CEOs shouldn’t cut evenly. “Remember, when you reboot a computer, it doesn’t usually reboot to the same state. Don’t feel as though you have to trim equally across eng, ops, sales and marketing,” he says.

- Keep a sales candle burning while you focus on product. Here’s how Jud Valeski saw it in the 2008 downturn when he was working on Gnip: “We went heads-down on the product. That product focus resulted in the realization that we were over-staffed to build and support the product we really wanted to build, so we let about a third of the team go,” he says. “We kept someone on the sales front in order to keep our fingers on the pulse of how businesses were reacting and adjusting."

- You might come out stronger — and with a new tattoo. “After Lehman in 2008, we immediately laid off a third of our company, which was around 60 people. It was hard at first, but the remaining team was amazing, and to my shock, we were able to accomplish a lot more with fewer people,” says David Hersh, the founding CEO of Jive. “2009 was the best year the company ever had — and we did it while putting cash back in the business. Right after the layoff, I told the company I would get a tattoo of the number 8 if we hit our $8M goal for Q4. We hit it. I still have it. I like what it represents — though I might recommend lowering the stakes and offering to do karaoke or something instead.”

Additional resources on layoffs:

- First Round Review article from Sam Shank: From Burning Millions to Turning Profitable in Seven Months — How HotelTonight Did It

- First Round Review interview with Beth Steinberg: How to Lead and Rally a Company Through a Layoff

- Video from First Round CEO Summit archives: The Taboo Topic of How To Do a Layoff

- Andreessen Horowitz blog post on Planning and Managing Layoffs

- Twitter thread from Alex Miller with a step-by-step guide for doing layoffs remotely.

- Carta's CEO published the candid speech he delivered at an all hands meeting detailing the company's layoffs.

PART 6: HOW TO BRING IN MORE CAPITAL — TIPS FOR PUTTING MORE FUEL IN THE TANK

Here are three strategies for extending your runway through addition, not subtraction. (Note: We’ve ranked them in order from best to worst options.)

1. Bringing in more revenue from customers:

The advice we’re sharing with First Round companies:

When it comes to interacting with prospects and existing customers, every move can feel like it might be the wrong one. Bandwidth and budgets are limited, so you don’t want to be a burden, but you also want to shore up certainty in your sales pipeline as you adjust your projections.

There has never been a more critical time not to lose customers. Consider undergoing a complete customer review to understand the health of your customer base. For many enterprise companies, the reaction of customers is all over the place. Some want to deepen partnerships, while others are freezing everything. Bucket each customer by potential risk of churn, and look at this dashboard every week.

Focus on getting paid upfront from your stickiest customers. Especially if you’re a SaaS business, ask for pre-paid contracts and give discounts to get them. Push the sales team hard to get pre-payments of 12 or more months, and reward them with bonuses for doing so. This is your cheapest form of funding.

Learn from your customers as much as you can. They’re likely focused on their own survival, so understanding how this is affecting them is key. Rework your positioning as much as possible in response. “Start with the person you're selling to. Understand their psychology and fears about survival. The best companies are able to reposition around what their buyers really care about, which is very, very fast ROI and taking costs off of their books, fast,” says First Round partner Bill Trenchard.

Advice from recession-era founders on revenue:

- Pitch a “buy instead of build” message. As Jud Valeski, formerly of Gnip, alluded to earlier, he saw the 2008 sales crunch as an opportunity to focus on the product. “We got to build the product we needed to build, without a ton of market distraction in the form of prospects telling us to do this and that with the functionality,” he says. “When we did emerge after several months of heads-down building, our message to the market certainly included how our product helped them save money. Many of our customers had laid-off engineers of their own, yet their business demands still required the functionality we provided. So, what they were once deciding to build, we were able to easily offer in a ‘buy’ package. Our pitch was deeply rooted in ‘It’s a good time for you to buy this stuff rather than take on the headcount expense of building it.’”

- Shift your mindset from “dollar-led growth” to “product-led growth,” says Jade Van Doren, former CEO of TechForward and AllTrails. “In bull markets, our focus as founders tends to be on growth above all else. Downturns force you to take on the harder challenges of building a more efficient business through product innovations, funnel optimization and organic customer acquisition channels,” he says. “While financially-disciplined growth through product and funnel improvement is often slower than throwing money at ads, the value of the business will be higher at any given revenue number because of the increased capital efficiency.”

- Go for more value over lower prices. “This is no time for business as usual. If you're sending outbound emails in an eight-email sequence, nobody cares. No one wants a 30-minute call with your SDR right now. They already had an excuse to ignore you before, now they really have an excuse,” says Gina Bianchini (of Mighty Networks and Ning). Many startups might focus on attracting new customers with freemium models or discounts, but she disagrees with that approach. “It may feel good at the time, but it can accelerate the death of your startup even faster. You may think you’re locking in value for later on with a free trial, but the conversion rate will likely be much lower than you expect with people who are used to getting something for free,” she says. Instead, think of creative sales and marketing efforts for the network you already have. “How can you restructure your packages to give the folks you already have relationships with a crazy amount of value for a premium price? Take this example: If you’re a hair salon, could you switch to an annual subscription model for haircuts and throw in additional products? This is the moment to go to anybody you have on the hook right now and make them a deal that they cannot refuse. You want cash upfront, and if you can get creative with what you’ll give for that over time, you might be able to strike a deal that’s a win for everyone (and before you do a massive layoff). If you come from a place of ‘I am grateful for our relationship. How do we get you more value?’ there will be a subset of your customers who will not just stick with you but fund you. It’s not going to be everybody, but at least spend some time on this effort before you start slashing prices.”

Get customers over the finish line with a “shock and awe” approach to delivering value.

Revenue tactics recommended by current CEOs in First Round community:

- Identify the two to three deals for each Account Executive that could close with a deeper discount.

- Offer more flexible terms, from a later start date to quarterly payments to opt-out options for a specific time period. It’s critical to retain the relationships, even if at a reduced level.

- Consider creating a hierarchy of different tiers of customer offerings: three years upfront prepaid contract, three years of annual payment, one year of annual payment, and so on.

- Share your company's business continuity plan and how you’re mitigating risk with prospects and renewals.

- Re-validate all of the basic elements of your engagements, from your customers’ priorities, to your solution’s impact, to who the buyers are — all of this might have changed.

- See if there are any customers you’ve built good relationships with whom you can go to for advice on how to handle the crisis or restructure your product offering. It may increase the strength of your relationship — and the chance that they’ll stick around.

Additional resources on revenue:

- Ad performance during COVID-19 analysis from Social Fulcrum

- Work-Bench’s Enterprise Sales Guide: COVID-19 Edition

- Harvard Business Review tips for brand marketing through the coronavirus crisis.

- Steven Forth, co-founder of TeamFit, outlines Pricing in a Time of Uncertainty.

- Camelot slide deck: COVID-19 — An Early Look at US Media Implications

2. Fundraise

In this decidedly-less frothy environment, many founders are questioning how rocky their follow-on fundraising path will get in the months ahead — and adjusting expectations accordingly.

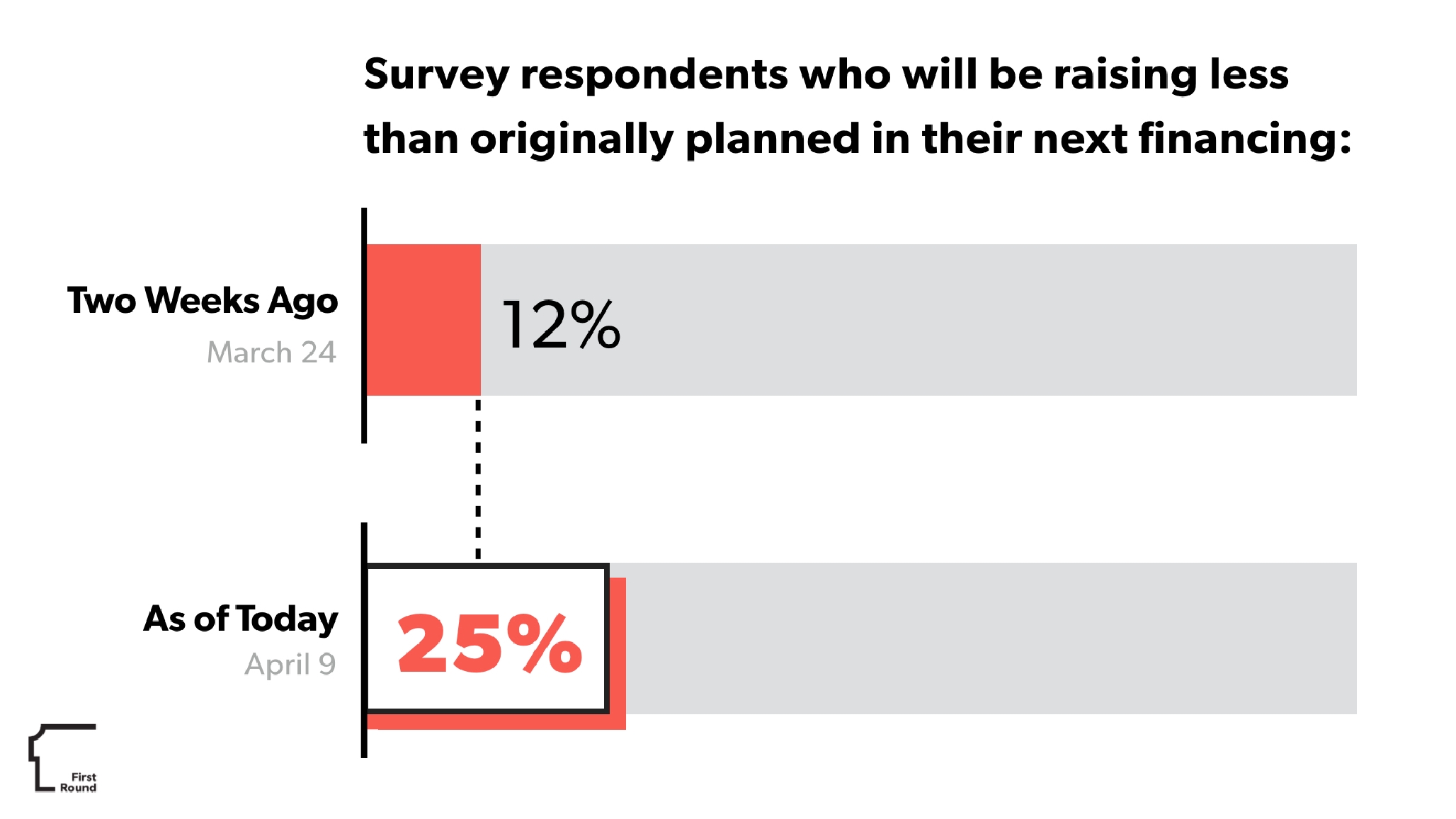

In our internal survey, we found that back on March 24, only 12% of the venture-backed founders we surveyed expected to raise less than previously planned in their next round. By April 9, that figure had doubled to 25%.

The advice we’re sharing with First Round companies on fundraising:

If you do decide to raise capital in this climate, remember the fundraising process could take much longer now. Plan for six months, not the shorter timeline that some startups have enjoyed in recent years. If you have an ability to raise at the same terms as your last round, consider that option (presuming that round was recent and you haven't dramatically outperformed). Raise on a SAFE at the last round price (as appropriate) and close the money quickly. Also, consider circling back to those who missed out. If there are VCs who wanted in on the last round but you couldn’t fit them in, reach out to them. You might also consider a top-off from a later-stage fund. While valuation is always important, comparable public valuations may be down by over 25% — so a flat round could be the new 25% up round.

These considerations aside, here’s the reality check Josh Kopelman is sharing with all of the founders he works with: “When you hear VCs saying that they’re still ‘open for business’ and writing checks, take it with a grain of salt. Pursue fundraising, but don't stake your business on a round coming together. In 2008, every VC on the planet said that. Yet if you look at the data, it tells a very different story. There was a greater than 50% drop off in overall venture funding from Q1 2008 to Q1 2009,” he says.

“In 2008, the average Series A company raised $4M on a $28.5M post. In 2009, it was considerably less with an average of $3.5M on a $14M post — half the valuation of the year before. And there were 30% fewer Series A rounds overall. So consider this backdrop as you talk to investors. On a daily basis, they aren’t just making a binary decision of whether or not to fund your company. There's a third decision which is, ‘Do I wait to decide?’ And I think that we should expect that a lot of investors are going to wait and see.”

In addition to funding sources drying up, the bar is also going up. “My experience is that during downturns, the yardstick changes. I explain it using a ‘Show me’ versus a ‘Trust me’ scale,” says Kopelman. “In boom times, it’s ‘Trust me.’ A founder says, ‘This is what I expect to do, and we're going to launch with bad unit economics, but in the future, it will get better,’ and investors will still cut a check — because they are willing to trust that the founder will be able to do that. During recessions, you're going to see far more investors sitting on the ‘Show me’ side. Founders will need to be able to say, ‘This is what I've done, here are my unit economics.’”

Advice from recession-era founders on fundraising:

Many recession-era founders felt fundraising efforts were unlikely to succeed and thus not worth the time. Matt Sanchez (of SAY Media) had a strong point of view here: “Don't waste time trying to raise money in the face of an economic event. Urgency, time pressure and uncertainty are all working against you,” he says.

Ning and Mighty Networks founder Gina Bianchini agrees. “If you assumed you were going to raise in the next few months, you’re not. You can’t grind it out and get there with 100 meetings. Right now, investors are a herd. They may take your meetings, but they’ll waste your time. They’ll all chase the markets that are accelerating. Your existing investors might also move the goalposts on you. You might have been trying to go big on a billion-dollar business because that’s what they told you to do, but now they’ll say they want profit and cash flow. That’s why you have to make these decisions as a founder based on your own values and beliefs, which is scary. So many VCs are saying the best businesses are built in recessions. That’s true — but what they don’t tell you is that it never feels that way when you’re in it.”

Not all shared this view, though. “We got a round done two days after Lehman ‘sold’ for $200M,” says Seth Sternberg (of Honor and Meebo). “I was too naive to know that should have been impossible to get done. Crazy things can still happen if you just keep pushing and are willing to hear ‘no’ a lot.”

If you are able to get close to the finish line, do everything you can to get it done. “I had a signed term sheet right before Lehman fell,” says Alex Rampell (current GP at A16Z, previous CEO/co-founder of TrialPay). “I recall a heated negotiation with the partner post-term sheet, pre-close where he said ‘Why don't we see how much the Dow goes down tomorrow and discuss?’ I quickly shut up. Don't get cute on deals — just get them done.”

Oren Michels of Mashery offers a similar piece of counsel. “If you let your ego demand a high valuation when times are good, it will be very difficult for you to get funded when times are bad,” he says. “Having been through two of these downturns — I launched my first startup five days before 9/11 — I have seen high valuations kill a lot of companies. A CEO I know recently received a term sheet and (with the support of their existing investors) actually negotiated to have the pre-money valuation reduced by 20% from what the VC firm offered. That is healthy long-term thinking, and I really respect him for it.”

Additional resources on fundraising:

- Kauffman Fellows blog post: This is how much harder it is to raise capital during a downturn

- PitchBook Q1 2020 Analyst Note assesses what’s in store for VC firms in the wake of coronavirus

- Dorm Room Fund’s Remote VC Pitch Checklist

3. Look into venture debt options.

In general, most recommend raising equity instead of debt whenever possible. Treating debt like equity has potential negative unintended consequences, particularly in a downturn or if you’re a pre-product/market fit company. If you do decide to pull down venture debt, read your material adverse event clause (MAC) and understand it.

Here’s what Oren Michels (of Mashery) had to share here: “If you’re not cash flow positive, venture debt usually isn’t a great way to extend runway — so don’t expect to be anytime soon. You generally have to take down the money long before you need it, at which time you are using the money you borrowed to pay interest — and then you come out of the economic crisis with a massive monthly principal and interest payment. Should things not recover as quickly as you hope, it’s hard to cut back to a cash flow positive budget if you have to make debt payments,” says Michels.

Like any other bridge, venture debt should be a bridge to somewhere specific, or else you can wind up giving the keys to your company to the bank.

PART 7: SUPPORTING YOUR TEAM AND LEADING THROUGH A CRISIS

In this section, we share advice for leading through uncertainty, taking care of your team and staying connected amid the shift to remote work:

Leading through uncertainty:

“This is a time where everyone is going to be tested. As a startup leader, you'll be reinventing everything. If you're still hiring, you need to figure out interviewing over video conferences. If you’re doing layoffs, you’ll be struggling to figure out how to do that empathetically over Zoom. How do you bake culture in? How do you deal with all of this uncertainty? How do you manage a sales team who has an incentive comp plan? There's just so much reinvention that’s required,” says First Round’s Josh Kopelman.

Clearly articulate the challenges your company faces to your people. People hate being spun, particularly in hard times. “It’s a founder’s job to balance transparency and hope,” Kopelman says. “On the one hand, it's important to be realistic and transparent with your team. You don't want to keep secrets. Founders must maintain their credibility, especially in a crisis. You can recover from making a lot of mistakes — but you can’t recover from a loss of credibility. You don't want to say everything's going to be fine if it's not. It's okay as a founder to say, ‘I don't know,’ or to say, ‘Here's what I'm concerned about.’ But you also have to recognize that your job is to maintain hope at the same time. You need to be sure to tell them that even if the waters are choppy, the destination will be worth it. If you don’t provide both in a crisis, it's a failure of leadership,” he continues.

“So if you’re in a market that’s affected, it’s important to say, ‘There’s not going to be much demand for what we have to offer this year.’ That's transparency. But the glimmer of hope could be, ‘But I actually think that when we emerge from this as a national player, we have the strength in the brand to recover and a lot of our smaller regional competitors won't.’”

Here’s the hard truth: You’re going to be tested in ways you can’t even imagine. This is a time to step up and thread the needle of staying transparent while still offering that glimmer of hope.

Howard Katzenberg — who was coming up through the ranks of American Express during 9/11 and OnDeck in the Great Recession, respectively — leans on a similar principle. “What I saw in Ken Chenault’s leadership after 9/11 was really moving for me, and it has continued to be the guiding force for how I think about leadership in these times,” he says. “Ken always repeated that his job as a leader is to define reality and give hope. Defining reality means explaining the situation, even if it’s very harsh. But at the same time, give hope by laying out the vision. Where are you going? What are the strategies and tactics that will help you overcome these challenges? Share why you’re excited about the plan without providing false hope. And then give them metrics by which you'll measure your success.”

Scott Weiss was leading IronPort during both the dotcom bust and 2008. Here’s what he had to share on how leaders can meet the moment: “Be extremely visible, engaged and on top of your shit. Everyone is looking for leadership during a crisis. You need to be making sure you’re the first one in, last to leave, making tough decisions and spending the extra time calming nerves and motivating,” says the former Andreessen Horowitz partner. “This is a make-or-break moment — and when the CEO needs to show up. Don’t be afraid to push the team, but compensate them and be there with them for every late night and weekend. This isn’t about doing more with less; this is about survival as a company. At IronPort, we gave out stock grants for 6-12 month pushes based on meeting our goals for shipping code.”

Leadership tactic recommended by current CEO in First Round community:

- One way to help build trust with your team is to allow them to dig into the unknowns, the downside and the upside on their own. As a team, do premortems and backcasts. That way, the team has produced the downside and upside scenarios and can come to terms on their own with the uncertainty. You can tell them you don’t know and things might be bad. But showing them by letting them work it out for themselves is a good way together. it will also increase the cohesion of the team and increase trust at the same time. Additionally, the data that comes out of it will be useful for getting ahead of how to deal with the uncertainty.

Additional resources:

- Harvard Business Review’s article asks Are You Leading Through the Crisis...or Managing the Response?

- First Round Review’s article: Crisis Management — From the Man Who Helped Save eBay

- Twitter thread from Suhail Doshi, former CEO of Mixpanel, on how to survive a recession as a startup

- Twitter thread from Avichal Garg, founder of Electric Capital, shared his lessons on running a startup through 2008

- Stewart Butterfield's Twitter thread on the behind-the-scenes process of moving Slack’s 2,000+ global workforce entirely remote

Taking care of your team:

Going through hard stuff brings teams together. It’s remarkable what humans are capable of and how resilient teams can be. But don’t overlook the toll it’s taking. Consider all the ways big and small that you can show how much you care. Don’t forget to celebrate your team and show how much you value them.

Finally, don’t change your stripes, says Simon Khalaf (currently Twilio, former CEO of Flurry Analytics). “Maintain the culture of the company. Don’t change who you are because the world is changing. Startups succeed because they want and will change the world, and not because the world changes them.”

Tactics recommended by current CEOs in First Round community:

- In Zoom meetings, go around the room one by one and get each team member to share an update on how they’re doing personally.

- One CEO noted that no one on the team is taking any time off, given shelter-in-place guidelines and limited vacation options. Remind your team vacation days are still available and encourage them to put it to use, even if it’s just on a few days relaxing and unwinding at home.

- One First Round founder shared that his startup hired a freelance writer on Upwork to interview the team members, writing the story of each of their lives and sharing one with the entire company once a week.

- Another CEO shared how they’re comforting the sales team, which is obviously uneasy as their sales quotas hang in the balance: “I’ve changed our sliding scale quota attainment program (which started at 50% of quota attainment) by getting rid of the floor. So, salespeople get paid regardless of the percentage of attainment, even if it's only 10% of attainment, they'll still get paid 10% of the quota. This may or may not matter, but at least it makes them know that we're on their side,” says the founder.

Additional resources:

- Pulse check how your team is doing with a few questions from CultureAmp's COVID-19 survey

- Harvard Business Review article: What Your Coworkers Need Right Now is Compassion

- LifeLab Learning’s People Leader Resilience Playbook: How to manage anxiety across your organization

- HRwired created A Guide to Navigating Grief and Loss

- HBR article: That Discomfort You’re Feeling is Grief

Staying connected amid the shift to remote work:

CEOs are now searching for creative ways to keep their teams connected and strengthen employee relationships amid a sudden shift to 100% remote work. Communication is key to that mission.

“In times of crisis, one of the best things you can do is just to communicate. It's the weekly fireside chats analogy from World War II. The regular cadence of communication to a team that is nervous and scared is really essential, and the best CEOs are laser-focused on increasing communication frequency across their team,” says First Round partner Bill Trenchard. “Employees want more metrics and more information than ever before. In an uncertain climate, many employees can't get enough of what used to be boring, in-the-weeds updates.”

Advice for keeping your team connected from recession-era founders:

- Over-communicate as much as possible, says Matt Sanchez, co-founder and CEO of SAY Media. “Everyone is anxious and the more isolated people feel, the more they shut down emotionally. Even bad news helps ground people in reality and connects them to whatever solution you have to navigate as a company,” he says. “We did weekly open forums with anonymous questions through previous crises and are doing them again now.”

- Completely change your cadence. What or how often you communicated should be completely different from a month ago, says Gina Bianchini. “I’m in every standup meeting right now, even though I don’t have to be. That’s my time to connect with my team. At Mighty Networks, we’re fortunate to be in a market that’s accelerating, but remember that it may not feel that way to your employees. Remind them that we’re in for pain and stories of failure, even if we are relatively fortunate. Clarify the ways that what you’re doing is important at this moment. For us, I’m focusing on how virtual connections are more important than ever. Communities allow people to do things together they can’t do on their own.”

- Be realistic. “My experience is that people don’t want to be sold on the ‘world-changing vision’ so much as they want to trust leadership to steer things in the right direction. War-time changes expectations, so be realistic about goals while keeping people’s attitudes up through lots of interaction,” says David Hersh, founding CEO of Jive.

- Go beyond the usual suspects. “I always advise people on my team to go two layers down. Don’t just check in with your immediate reports, check in with their immediate reports one-on-one as well,” says Howard Katzenberg, formerly of OnDeck and American Express. “Ask them how remote work is going for them so far. Reinforce that it’s okay to have doubts or anxiety and show some vulnerability by sharing your own.”

Communication tactics recommended by current CEOs in First Round community:

- Start sending a weekly CEO letter to share your views on what happened last week.

- One First Round CEO has moved to daily revenue forecasting in an effort to get “crazy transparent” by sharing every bit of data. “It produced a big change in culture — people are intensely motivated by every drop in revenue,” the founder says.

- Ramp up the cadence of your standups and All Hands. Some First Round founders have moved to daily standups that go over all the numbers or get deep into the weeds: cash on the balance sheet, securitization and capital markets.

- Send out Google surveys before meetings to gather anonymous questions that everyone has, but no one wants to ask out loud.

Script and practice all internal communication. Your words matter more than ever. Get the team focused on the hill you’re going to climb and the challenge ahead.

Additional resources:

Remote work:

- First Round Review article: Struggling to Thrive as a Large Team Working Remotely? This Exec Has the Field Guide You Need

- GitLab, the world’s largest all-remote company, published The Remote Playbook

- HRwired crafted a guide to navigating distributed work

- LifeLabs Learning compiled tips on remote work for employees, managers, and people ops leaders

- Knowable created a new course on working from home (during a pandemic)

- Mathilde Collin, co-founder and CEO of Front, wrote a Medium Post: 25 things we’ve implemented at Front to keep a great culture while being remote

- Julie Zhuo’s newsletter on managing remotely

Internal comms and policies:

- LifeLabs Learning ideas, policies and templates for HR & People Ops navigating COVID-19

- Internal communication best practices and an example from Abstract

- Harvard Business Review article: Communicating Through the Coronavirus Crisis

- First Round Review: Staying Connected is Key to Your Startup’s Survival — Here’s How to Nail Internal Comms

PART 8: ENDING ON A HIGH NOTE — THE UPSIDE AND THE NEXT WAVE

Today’s environment can derail even the most well-established self-care practices and mental health habits. Here’s a collection of thoughts on how to look for the bright spots that seem hard to find.

Advice from the First Round team:

To shine a light on potential and reframe your mindset, ask yourself: What are the unexpected opportunities that have come out of this chaos already? Look for them everywhere: the market, your customers, your team, your personal life.

Remind yourself that while we may be seeing more uncertainty than ever before, many great companies were built during uncertain times. “Back in 2008, I had just started becoming very active in seed investing,” says First Round’s Bill Trenchard. “Two companies really stand out from that period. One is Uber and the other one is Lending Club. In both cases, you had founders who saw structural changes in the economy. The best founders will sort of see where the world is going. And that’s not about making infallible predictions, it often just means riding the wave of a big trend, like slack labor markets or the hunger for alternative financial products after the banks collapsed. Every time you have one of these bombs go off in the economy, which seems to happen about every ten years, it resets the table.”

As for how things might get shaken up after this particular crisis, Trenchard shares a few guesses: “As I look ahead, I think the government's going to have a bigger role in our lives in the next ten years than it did in the last ten years. Understanding how government as a customer — how it works and what its needs are — might be a valuable place to mine. We're also having a mass dislocation of part-time workers again. Take the time to think through what’s going to change as a result of these shifts, how you can get smart on it and what opportunities might be opening up.”

These disruptions also cause a significant change in the profile of folks who are willing to take on new company-building challenges. “The risk thermometer changes,” says Josh Kopelman. “People are willing to embrace more risk with each year of boom — on both sides of the coin. So on the heels of 10-12 years of boom time, venture investors were willing to fund a lot of risk in 2019. As a result, it was easier for typically risk-averse people to become founders because there was a good chance they would get funded. But risk tolerance shifts very quickly in a recession,” he says.

“Now, only the heartiest of founders are likely to start companies, and ‘the tourists’ or ‘hobbyists’ will go home. To start a company now, you have to be so passionate in yourself and the idea because you know that it's going to be so much harder. It's the difference between saying, ‘I'm going to drive 10 miles in my car’ versus ‘I'm going to hike10 miles in Antarctica.’ The environment you're taking your trip in impacts the difficulty and odds of success — and the profile of the person setting out on the adventure.”

When it comes to who will be starting the next wave of great companies, you’ll see far more Arctic explorers than joy riders.

Advice from recession-era founders:

Let’s end on some words of inspiration from founders who’ve weathered downturns and come out stronger on the other side.

“I’ve experienced my biggest breakouts during recessions,” says David Hersh, formerly of Jive. “If you are lean, disciplined and purposeful, you can achieve amazing things with a smaller group of people on a mission, while all the other companies are hunkering down or shutting down.”

Specifically, it helps to be on the lookout for secondary and tertiary impacts, says Jade Van Doren, former CEO of TechForward and AllTrails. “Downturns often create unexpected opportunities that are unrelated to the primary impact of the shock. For example, with TechForward in 2008, the real estate bubble bursting created a financial environment where consumer electronics retailers could no longer afford ‘business as usual,’ and had to be more open to new ideas, which benefited us,” he says. “Similarly, some of the most interesting long-term impacts of our situation today may be well outside the fields of healthcare. A secondary impact might be the mandatory remote-work environment that many of us are currently experiencing. Perhaps a tertiary impact could be the unprecedented opportunity to create online communities that foster connections across the world.”

And don’t forget to play offense. “Probably 75% of the playbook is playing defense right now — but 25% should be figuring out how you can play offense,” says former OnDeck CFO Howard Katzenberg. “In 2008 at OnDeck we were competing with the merchant cash advance industry and a bunch of shady operators were getting their leads through the broker channel. And then when the crisis hit, 80% of those providers went away. So we stepped in and tried to treat the brokers really well, paying them nicely to secure the relationship. When the economy turned around, we were suddenly the first look for a deal.”

Hiring is one space for opportunity. “Keep an eye out for opportunistic hires if you can. Back in the dot-com era, I was able to build an amazing team,” says First Round’s Bill Trenchard. “Lloyd Tabb and Jim Everingham were incredible steals for me back in the dot-com era. A huge benefit from the downturn was that there were just incredible people available. For the past several years, the conventional wisdom was that you couldn’t really pull together teams like that anymore, there was just too much competition for talent. But I think it will be possible again.”

Mighty Works founder Gina Bianchini agrees. “Can you change your business model to support more people? If you can, this is a great moment to raise the bar for the people on your team. You can recruit in a way that you couldn't recruit three weeks ago,” she says. Scott Weiss, former Andreessen Horowitz partner and IronPort CEO, has an apt metaphor here: “This can serve as the impetus to upgrade your team. Think as though you’re the owner of a successful team in the NFL and six teams suddenly go bankrupt,” he says. “Your starting lineup is about to change.”