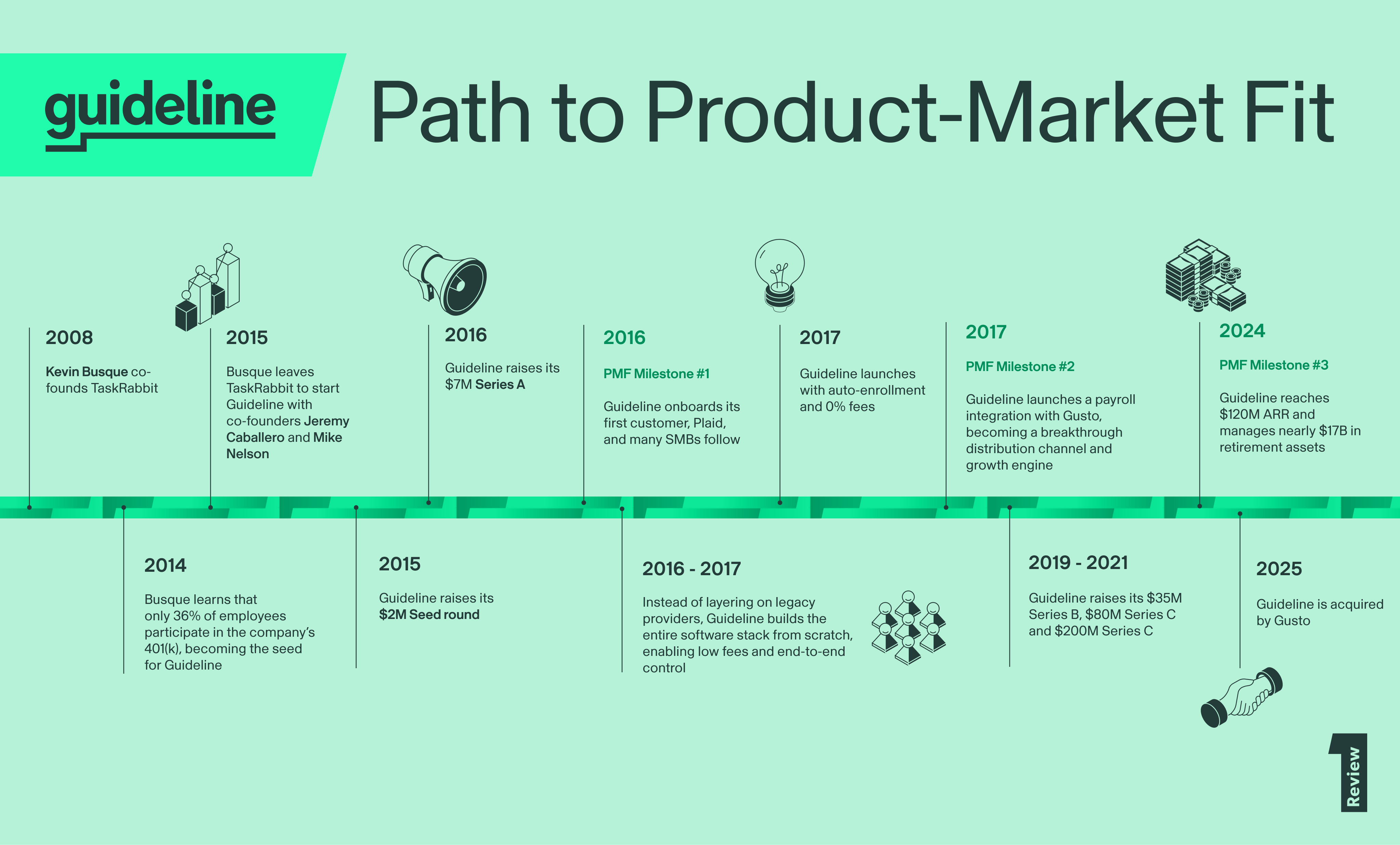

It’s 2014 and Kevin Busque is too busy to be verifying 401(k) contributions on every pay period. As co-founder and VP of Technology of TaskRabbit, the same-day service platform widely credited with catalyzing the gig economy along with Uber and Airbnb, he is focused on scaling the company rapidly. TaskRabbit recently launched in London, its first international market, and its headcount has grown to 70.

Compared to his days as a scrappy early-stage founder, figuring it out on the fly with a small band of early hires, things now look very different for Busque. He spends a lot of time thinking about leadership. Thinking about hiring. Thinking about HR and employee benefits. It’s the latter in particular that begins to keep him up at night, after he stumbles upon a discovery that makes him do a double take: a mere 36% of TaskRabbit employees are enrolled in the company’s 401(k) plan. It doesn’t make sense.

“I remember the number, because when I found out, I was flabbergasted,” Busque recalls.

He begins trying to understand why so few of his employees are making use of this company benefit, which costs TaskRabbit more than $20,000 annually. As he takes a closer look at their 401(k) providers, he starts to grasp the issues: clunky, outdated systems, a lack of integrations, confusing (and often hidden) fee structures. It’s no wonder so many TaskRabbit employees have decided it’s all too hard. His founder’s brain is itching, seeing the problem as a challenge. He becomes obsessed with solving it.

Retirement funds for SMBs: Not the sexiest market sector to tap, necessarily, but one that was begging for someone to come and shake it up.

Cut to August 2025. Guideline, the billion-dollar company Busque co-founded with fellow TaskRabbit alums Jeremy Caballero and Mike Nelson in 2015 to make 401(k) simple for SMBs enters a deal to be acquired by HR tech giant Gusto, Guideline’s long-time payroll partner, founded by Tomer London, Joshua Reeves, and Edward Kim (whose path to PMF we've also cataloged here on The Review). It’s a move that has been celebrated by both companies as the natural next step in their long-standing partnership, and a win for the thousands of small businesses they serve together. Busque describes it not as an ending for Guideline, but the beginning of a new chapter.

So, what happened in between those two points on the map — from Busque’s first inkling that 401(k) for SMBs needed fixing, to acquisition? What does that journey look like in hyper-detail? In a recent conversation, Busque opened up about how he made the decision to leave TaskRabbit and plunge into a new venture, why it was crucial for Busque and his co-founders to build their full software stack from scratch, the advice that helped them find product-market fit and more.

Let’s dive in.

When traditional providers ignored SMBs, Busque noticed the gap — and the opportunity

When Busque first squinted at that 36% figure on his screen and realized there was a disconnect between the 401(k) offering at TaskRabbit and actual employee participation, he began to examine their benefits program and found himself surprised — and frustrated. It wasn’t just that the company was pouring money into a perk only for it to be ignored by the majority of employees. It was the inefficiencies Busque uncovered that almost drove him mad.

“At TaskRabbit, our payroll and our 401(k) weren't integrated, even though they came from the same company. That was mind blowing to me. Why am I validating contributions after every pay run?” he remembers asking himself. “This should all be handled in the data set in the product.”

Then there were the fees.

“In the 401(k) legacy ecosystem, there are middlemen that charge asset-based fees: your record keeper, your TPA (third-party administrator), your fund investment manager,” says Busque. “The pricing is incredibly opaque. Often, you don’t know who is paying the fee — the company or the participant. I started digging through them all, trying to understand what an asset-based fee really was. Essentially, it’s a lot of people who are not adding value to your 401(k) plan, but are still getting paid for it.”

Busque began to search for an alternative to TaskRabbit’s 401(k) provider.

“Fidelity didn't want to talk to TaskRabbit,” he says. “We had 70 employees and zero assets.”

The SMB opportunity was being ignored completely. That was the precipice: I’ve got to find something better than this. I didn't find it.

Many founders will recognize the terrain Busque describes. You can’t find the thing, because the thing does not yet exist. It was clear to him then that SMBs were in desperate need of an accessible, affordable, modernized solution for retirement funds, especially 401(k).

“I wasn't knowledgeable about it, but I started digging into it. Previously I was a data engineer in the healthcare space. I figured I could come up with an angle to make this a better experience.”

Still, the prospect of entering an industry in which he had no professional experience, especially a sector dominated by an old guard of long-standing legacy brands, was daunting. But Busque was buoyed by words of wisdom from his grandfather: “When you thoroughly understand something, there’s nothing to it.” If he undertook deep research, did his due diligence, Busque had faith he could build something valuable in the gap in the market he’d identified.

While still at TaskRabbit, Busque spent almost two years doing in-depth analysis of retirement fund fees and inefficiencies, as well as familiarizing himself with the IRS code and SEC and Department of Labor regulations. He realized that if he wanted to solve for the major flaws in 401(k) offerings — especially hidden fees that siphon-off savings — he’d need to build an extremely complex product. Also, it would have to be built from scratch.

“If I was going to be able to deliver a differentiated product, it was going to be completely vertical. I was going to own the entire software stack,” he says. “That was important for product-market fit for Guideline, because if we had to go back to the small business owner every two weeks on a payroll run and ask them to validate all this stuff, that's a ton of work that they don't have time to do. That was a key insight into developing the product.”

To verify his idea, Busque sought the opinion of Zachary Perret, co-founder and CEO at fintech company Plaid (spoiler: Plaid would become Guideline’s first customer).

“I went to Zach because I wanted to do something at Guideline that could either mimic Plaid’s investment philosophy, or at least take into account that philosophy, so I could do something that was additive to it,” says Busque.

Perret was enthusiastic, telling Busque, “‘I want that product.’” It reaffirmed Busque’s vision.

The product decisions that gave Guideline its edge

Busque approached Nelson and Caballero, then TaskRabit’s Lead Product Designer and Staff Engineer respectively, and told them about the idea. Nelson and Caballero were natural confidantes. The three had been working together closely building a product focused on sourcing laborers for hourly work, in partnership with another company, which would be branded separately from TaskRabbit (it was eventually killed due to a reorg within the partner company), unexpectedly leaving the trio feeling adrift. Busque made the call to leave TaskRabbit so he could focus on his new project full-time.

“I knew I was going to do something different at some point,” he says of making the call to leave. “It was a slow build, and then it just felt the right time for me to go out there and do my next thing.”

His first priority? Fundraising.

“I don’t believe in stealth mode,” Busque explains. “Everybody has ideas. For me, it's always about execution.”

The co-founders began trying to raise their seed round. "I needed to raise capital to pay employees to come build this thing with me," Busque says. Because they'd be creating a product that owned the entire software stack, this wasn't something they could bootstrap. With his success at TaskRabbit, there was guaranteed interest in Busque’s next venture. There was no doubt that he would be able to get in front of the right people. The only question was whether he could convince potential investors of its value.

"We had to be able to prove this problem exists.”

Busque and his co-founders built a tool that estimated fees individuals were paying out of their 401(k) — fees they were often unaware were eating away at their earnings, which they would demo at meetings with VCs.

“You could look up someone’s 401(k)s, figure out how much they were paying and make it personal — take it to an individual and show them how much money they’d be losing over the next 20 years, often $400,000 to $600,000. The difference between 1.6% basis points and 8 basis points is a ton of money.”

Seeing the potential investors’ eyes widen at how fees were eroding retirement savings affirmed Busque’s belief that Guideline had strong potential for product-market fit.

Early on in the fundraising process, Busque was pitching a product that was more all-encompassing in the benefits space than just 401(k). But this approach, one VC said, was a mistake, and they opted to pass (but they would eventually come back for the Series B and write the lead check).

Some advice the firm gave would prove pivotal. “They gave the feedback, ‘You're biting off too much. You need to focus on one thing,’” he says.

Busque took this seriously. And it was this decision to narrow their focus, along with the choice to build their stack from scratch to save costs at the participant end, that would eventually secure Guideline’s path to success. Busque had heard about others who were exploring the 401(k) for SMBs space, too. But they weren’t going as deep.

“If I want to bring you a modern 401(k) experience, I can go about it in different ways,” Busque says. “The basic one is to put a flashy front end on it and use all of the legacy institutions behind the scenes. I'll go get a census for a record keeper. I'll find a third party to administer the plan. I’ll pay a record keeper. I'll only do the front end software, then I’ll tack on an asset-based fee.”

But from his research, Busque knew this approach would rely on external vendors and middlemen, who would add on their own fees, which would contradict the very problem he was trying to solve. He was well aware the others might have been able to move faster, but their product would not be as holistic, or effective, as Guideline. He remained committed to doing it the hard way, maybe taking a little longer, but getting it right. Nelson and Caballero agreed.

“I said to Mike and Cabs: if we're gonna do this, we need to start at the bottom. It's gonna be boring. We're gonna spend a year building record keeping. But it will give us this advantage all the way through, because we don't have to charge asset-based fees like everybody else does,” he says.

We went up the stack from the bottom, all the way until we delivered an end product on a web experience. That was super important — it gave us the advantage we needed.

Guideline became their own first customer. “We were eating our own dog food, which was super important — what did we want in the product?” Demand mounted while Busque and his co-founders were still in this pre-launch phase. “So many people that I was talking to were like, when are you launching? When can I have this?”

Plaid was the first to come knocking, after Busque’s conversations with Perret early on. “Zach was adamant: if you’re not going to do this now, when are you going to do it?”

Determined to ride the momentum, in December 2016 they launched Plaid’s plan before the product was fully operational. This meant it was a more manual process than they would have liked. “At that time we were outsourcing to a third party to do checks. We called it a non-integrated plan, or NIP. We still have a few of those today for the bigger plans that have a homegrown payroll, or something like that.”

But it also enabled them to build a better product. “That was really important, to get in the weeds, productize the process, and bring it back in-house and develop it in software. Luckily for us, Plaid were great about it — if there was an issue, we would work with them on solving it,” says Busque. “Keeping up with Plaid, we called it the ‘Plaid problem.’ It enabled us to go upmarket. It was important to get up and running that first year, because then we had to do 5500 filing and integrate with the IRS shortly thereafter, to keep those plans in compliance.”

More early customers followed. There was TaskRabbit (no surprise there), as well as some mom-and-pop SMBs, like cupcake shops and bakeries — the exact kind of businesses Busque had in mind when he decided to fix 401(k).

Busque’s pioneering approach extended to every aspect of the product. In what was considered radical when compared to industry incumbents, Guideline launched at 0% AUM (assets under management).

“People couldn't believe we could do something like that,”he says. “The truth is, it was very difficult. But we were in early startup mode and didn't need to make a profit. We just raised the seed.”

It’s a good example of how you can, with meticulous market research, come to understand what people most dislike about your industry incumbents, and how to exploit those weaknesses to offer a truly differentiated product. As Busque has shown, digging deep into the research to understand the nuances of the industry you’re in pays off.

Another example is Guideline’s approach to enrollment. Up until then, 401(k) plans typically required that participants opt-in. Busque was convinced this was part of why enrollment rate at TaskRabbit was low; there were myriad reasons that might prevent a new employee from signing up to a 401(K), such as miscommunication during onboarding, or uncertainty about the product. That’s why a core feature of the Guideline product, from the beginning, was auto-enrollment. Instead of requiring employees to opt-in to the 401(k) plan, they would instead be automatically enrolled, but given the option to (easily and quickly) opt-out.

This was a non-negotiable for Busque.

"Automatic enrollment was one of the earliest decisions we made. If you do nothing, you're going to be in the 401(k) plan. You get a target day fund and a set contribution rate. You're invested automatically.”

It seemed radical at the time. But his foresight would be proved prescient a decade later when the Secure 2.0 Act mandated auto-enrollment for new retirement plans in 2022, enshrining as policy what Guideline had championed from day one. It’s a reminder that true innovation often feels uncomfortable at first, but can lay the groundwork for lasting change.

It’s also a lesson in building for the needs of your target audience and being willing to forget the rest, even when appealing to a broader market might be tempting. Busque estimates the auto-enrollment feature led to the loss of “perhaps five or ten plans out of the first 100.” But in the end, it became a defining characteristic of the product that set Guideline apart, and, in what is perhaps the ultimate validation, was adopted by other retirement funds in the years to come.

Busque is unwavering in his view that when it comes to making product decisions, it should always come down to relentless focus on participant outcome.

“Stay true to who you are,” Busque says. “I had a lot of conviction that this was the right thing to do. If you didn't want to participate, you could get out of it with the click of a button. But we have so many notes from people saying, ‘Thank you for putting me in. I didn't have time to do it. I've been in it for three years and I've made 30%.’”

Busque had confidence in his product. He also knew they would not be able to rely on word-of-mouth alone. So, they made a few sales hires who began outbound. This was an area where Busque admits they “failed,” though it would result in crucial early lessons that ultimately got them on the right path.

“We brought in a few sales folks,” he recalls. “I was like, ‘you guys sell 10 plans this year. I will take you to Mexico. We didn't sell 10 plans. Nobody went to Mexico.’”

The issue was tied to what Busque mentioned about needing to tell the story of the problem Guideline was solving. They came up against misunderstanding among the customer base. Folks lacked a deeper understanding of just how bad fees on 401(k)s were, or seemed dubious that providing a 401(k) was even possible for an SMB owner.

With around 60% of customers signing up on their own, Busque leaned heavily into product-led growth and opted not to invest further in building out a larger sales team. “In hindsight, do I wish I’d hired a sales leader to get that other 40%? Absolutely. I regret it to this day.”

You could say it was a lucky mistake. It forced Busque to find an alternate solution to sales-led growth, resulting in a partnership that would be transformative — and also lead to Guideline's acquisition a decade later.

How a payroll integration with Gusto helped scale Guideline to tens of thousands of SMB customers

“Where do people look to bring on new benefits?”

This is the question Busque asked himself after the “failure” of the outbound sales efforts. How could they reach the right people, at the right time, and find the customers he knew would benefit enormously from using Guideline’s product? The answer eventually came: a payroll company.

The realization led Busque to Gusto (previously ZenPayroll), a service that had been using software solutions to simplify payroll for SMBs since 2011. Together, Gusto and Guideline built an integration that allowed Guideline to tap Gusto’s customer base, as well as feature a product display in the benefits tab on the Gusto website. Busque defines this moment as the big unlock that changed everything.

“We built this whole ecosystem with them, and they became a customer. The integration gave us operational excellence and scale. It was good for Guideline, but also for Gusto; it's a 100% margin business for them.”

Not only could they increase customer acquisition this way, but the integration meant that if a Gusto customer signed up with Guideline, Guideline could ingest the customer’s payroll data, vastly simplifying the process at the user’s end. It was a 360-degree integration which meant if the customer changed their contribution on Guideline, it would also update in Gusto, and vice-versa.

“It allowed us to get to the scale that we are,” Busque says. “92% of all of our customers are on an integrated platform. That's where we play really well. We're 400 people at Guideline, but we service almost 60,000 small businesses at this point. If you look at any other competitors like ADP, that are at our scale, they have hundreds and hundreds of people just servicing 401(k). We do it all in the system.”

A decade of partnership becomes an acquisition

The possibility of Gusto acquiring Guideline was there from the beginning.

“Since as early as 2016, Tomer and I had been having a recurring conversation about it,” Busque says. “I was open to the idea, but first I wanted to prove Guideline in the market.”

Talk turned serious in the spring of 2024. “It was a Goldilocks moment,” as Busque puts it. Guideline was about to turn 10. The company had been profitable for 18 months, hitting around $175 million in ARR. Guideline had reached a strong, stable point. But sustaining the kind of growth expected of a VC-backed company was only going to get harder; Busque was beginning to observe consolidation in the 401(k) services space, and that companies would increasingly build or own their 401(k) products, reducing demand and putting downward pressure on the fees that could be charged for a product like Guideline.

Gusto wasn’t the only contender; there was interest from other parties. Guideline did their due diligence, exploring these other opportunities. But given Guideline and Gusto’s long partnership and deep integration, in particular their compatible tech stacks and high number of shared customers, it was clear Gusto was the most ideal acquisition partner. “They were our first partner, our longest partner, our fastest-growing partner throughout the history of Guideline.”

Alignment did not mean it would be easy.

“The transaction itself was incredibly complicated,” Busque says. What made the acquisition so complex was that Guideline, as a regulated financial services company, was not a single, simple business that could be cleanly transferred. The company was structured as multiple licensed and regulated entities under one corporate umbrella, including a record keeper and a registered investment advisor, each governed by its own compliance requirements.

To make the deal work, Guideline essentially had to be split into two parallel businesses: one serving customers integrated with Gusto’s payroll platform, and another serving customers using other payroll providers. That meant separating books of business, restructuring licensing agreements across entities, and ensuring strict data segregation, all while maintaining continuous compliance with regulators like the SEC, IRS, and the Department of Labor.

I remember looking around, like, ‘Is there a blueprint for this? Has somebody done this before? I couldn't find it.

Because Guideline had to be divided into Gusto and non-Gusto books of business — and because each part of the company carried its own regulatory and licensing obligations — different pieces of the deal had to be worked through simultaneously. While Busque was negotiating the terms with the Gusto team, other discussions were happening at the same time about where certain customers would go, how licenses would be reassigned, and how to separate systems without disrupting active payroll runs or delaying investments. It meant juggling several interlocking conversations at once, with three, four, sometimes five parties involved.

“Daunting,” is the word Busque uses to describe this period. “I didn’t sleep for months.”

This complex unchartered territory meant that the deal could have dangerously stalled, or fallen apart. Busque says what held it all together was the strong relationships underpinning the deal.

“It took a ton of partnership on both sides to get it done,” he says. “It was important to have that decade of experience with Josh and Tomer to get through this deal. Quite honestly, I don’t know if we would have got through it, had it been a new entity.”

Busque’s long-time rapport with his outside counsel, Andre Gharakhanian at Silicon Legal Strategy, who has been his attorney since the TaskRabbit days, was also crucial.

“It’s one of the things I relied on the most. Gharakhanian could reach out to ERISA attorneys [lawyers that specialize in the Employee Retirement Income Security Act of 1974] and people that know the SEC and the IRS, to bring that all together in a short window. We did it without bankers involved, which was kind of amazing.”

It’s his number one piece of advice for other founders going through an acquisition.

“Be careful who you choose for the professionals around the table. Make sure you have a solid relationship with them. Get referrals, get introductions. Do your due diligence. It's really, really important to get that right.”

For Busque, the acquisition means the mission he began building Guideline with — to fix 401(k) for SMBs — can continue to scale in a way that only a decade-long partnership could make possible. He believes it sets up a better experience for a new generation of investors, with more transparency, flexibility and fewer of the frictions that defined the old system.

“Gen Z is one of the fastest growing investing categories. Those people work at small businesses, too. They don’t just want mutual funds anymore. It’s important to make sure that we have an amazing investment suite for them. We can do that as one team under Gusto.”